Post #60: The road to serfdom

US$: 100.1; Fed’s B/S: $6.1trn; US 10-yr: 0.59%; S&P 500: 2789; Oil: $19.82; Gold:$ 1,736; Silver: $15.86

Below please find my “edited for post presentation” comments to Greg Hunter’s interview with Dr. Paul Graig Roberts, which was made available on youtube on April 14th.

Paul Craig Roberts – We Need Debt Jubilee or System Collapses

https://www.youtube.com/watch?v=cpi04VA1XQg&feature=push-u-sub&attr_tag=AnLXSY_hs3l6Y_d7%3A6

DK ANALYTICS

1 day ago (edited)

Thanks, Greg, for the interview. Frankly, I’m amazed by Dr. Paul Graig Roberts’ nationalization/debt forgiveness recipe as the only cure. When has nationalization of an economy anywhere in the world ever led to a good outcome for the majority of the people, be it in terms of freedom or economic prosperity? How can he de facto be willing to entrust the same lawless big wig scoundrels that are never committed of any crime or do any time to suddenly “grow a conscience” or to do what’s right for the supposed true sovereigns, the people. How naive is that? The bigger the government gets, the less constitutional it is, and the more cronyism and redistributionism and money printing there is. This is the opposite of letting the “system clear.” It is also at odds with human nature, free market incentives, the Invisible Hand of Adam Smith, enterprise, and thrift, the collective backbones of a wealthy and free society.

It also known as socialism, be it the fascist or the communist variety. Socialism IS the road to serfdom for vast majority of the population! Therefore, Roberts’ authoritarian recipe to finish off the little constitutional fidelity that’s left and to print the money to bail out the very corporations that he correctly said bought back stock, leveraged their balance sheets, and went overseas to produce is both inconsistent and conducive to yet more moral hazard. And, if we really want to bring companies back to America, let’s clean up our own backyard first, starting with massive reform of the very litigation and regulatory insanity that has long pushed lots of companies overseas in the first place!

Staying in the private sector that needs to be bailed out …. After Roberts’ recommended bailout of citizens via, I suppose, the Fed buying all the private household debt that can’t be serviced just like all the corporate debt that can’t be serviced (Wall Street always gets bailed out by the Fed taking junk bonds off its hands at way above market prices if the Treasury/the taxpayer doesn’t do it such as with TARP), is work incentive-killing, supply-withering, unaffordable universal basic income next? I ask this because you can’t issue a “nationalist, Constitution-finishing edict” that states that all the off-shored jobs and factories “have to come home” and expect a viable system of thousands of components suppliers to suddenly reappear “overnight” after decades of outsourcing!

And what will that universal basic income buy if the currency being issued hugely exceeds real GDP growth and becomes increasingly worthless thanks to even more money printing as foreigners ditch the dollar and the Fed’s balance sheet expands even more as it “soaks up dollars coming home” because no one else will? Plus, what happens to hurting creditors, very much including pension funds invested in bonds (about 40% of allocations) when, on top of a decade plus of yield deprivation run for the benefit of debtors, their bonds are suddenly worth only “50 cents on the dollar?” Is this not massively doubling down on moral hazard? And aren’t the real suckers the people that lived frugally, the companies that didn’t binge on debt but instead invested in organic growth, and the states that have managed their finances relatively well? Is this the right signal to send to those that tried to do the right thing, financially and economically? Hello!

Moreover, on the heels of such a debt jubilee or Fed assumption of non-performing/junk debt, what will the cost of money be, i.e., after the SAVERS/creditors get screwed royally, again very much including Main Street’s pension asset owners? How much pension income will they have on the heels of such a “jubilee” with which to buy anything? Instead of just having to sell their bonds and stocks because there are no coupons or dividends worth a damn, they won’t even be able to “burn their furniture to stay warm!”

Which creditor, with his suddenly “50% lower net worth,” will again lend money at 1%, 2%, or 3% after that, much less have any funds left to lend? How is this supposed to help encourage the very savings that will be necessary to rebuild America’s manufacturing might, which will take decades to fully accomplish, just as it took decades to lose (think Apple’s Jobs, who said he couldn’t do “relocalization” of Apple’s nearly exlusive Chinese/Asian manufacturing if he wanted to, because the manufacturing skills and the expansive requisite supplier base is nowhere to be found in America!).

Roberts’ “solution” is irrationality, much like continuing to bail out Wall Street and K Street cronies is counterproductive theft, i.e., highly destructive folly for 99% of Americans! Plus, it is also about as far removed from the very Constitution (clearly LIMITED and delineated government powers, separation of powers, sound money, federalism, extensive property right protections) that brought the country the greatest wealth and individual freedom ever known to mankind, which all happened prior to the creation of the Federal Reserve in 1913 and prior to the disastrous 16th Amendment (federal income tax) and the anti-federalism 17th Amendment (election of federal senators through direct votes instead of via state governments), all of which conspired to fuel a growing central government leviathan doing the bidding of the elites in DC (elected officials, un-elected bureaucrats numbering over 2m, and their crony pals on K Street and Wall Street) as enabled by counterfeit currency/the printing press.

That same “toxic public policy stew” has given us $1.9trn in annual regulatory compliance costs and litigation costs as a percentage of GDP that exceed Europe’s by a factor of nearly 3:1! All this has stymied the majority of Main Street entrepreneurs, who have long had to make extortionist payments to regulators instead of investing in organic growth, who have long been afraid to bring new products to market because of litigation fears, and who have long been prevented from expanding the payrolls or the salaries, as that money instead went to statist bureaucrats and their crony hangers on. Who wants more of this “business model” via nationalizing capital markets, nationalizing corporations, and nationalizing individual finances and income? Really?

Moreover, if Roberts is duly concerned with “forced vaccinations” courtesy of demented, power-hungry, “reduce the global population to 900 million people carrying capacity” Bill Gates and other such “lovely” people (e.g., Soros), who are pushing this Orwellian enterprise together with the government bureaucrats from Dr. Fauci’s CDC on down, how can Roberts possibly invest yet more trust into the type of tenured, sheltered, un-elected, un-representative, overpaid, power-hungry bureaucratic statists that are in bed with Wall Street and K Street kleptocrats pushing cronyism/fascism? BTW, members of this same “fine,” “fourth estate,” utterly unconstitutional bureaucracy have facilitated record student debt, record professor compensation packages and perks, “Rome, revisited” like college campus expansions, and destructive indoctrination instead of education. How can Roberts trust them or willingly EMPOWER such “technocrats” to “do the right thing” when it comes to a “debt jubilee” or any other totalitarian enterprise they engage in? And this from the “father” of supply-side economics? Wow, wow, wow!

How about trying revisiting the Constitution, from A to Z, instead, Dr. Roberts, and you’ll get your supply back and your jobs back and your wealth back, brick by brick, which will likely take the better part of a generation. And the only way to (re)start everyone’s engines is to open back up for business NOW! Since when has an influenza with an average death rate, when measuring the broad population, EVER given the authorities the despotic power to shut down most of the country – talk about the ultimate hollowing out of the 5th Amendment’s Takings Clause protections! (Never mind what this has done to civil liberties such as the 1st and 4th Amendment rights, i.e., the freedom to assemble and to privacy protections!)

In short, we have to revisit sanity, what works, and the real world. But please, Dr. Supply Side, do not advocate doing it through even more central planning. Let us not double down on the road to serfdom. We don’t need to go from bad to worse. To a full-fledged Banana Republic or to “Back in the USSR!” Good grief, who’d have ever thought … that the only viable allocation response was to include the ultimate insurance against such totalitarian policies, namely physical precious metals inclusion?

Ironically, and most sadly and destructively, the globally debilitating Corona virus “shutdown” response is hastening the day when confidence in counterfeit currency policy is overwhelmed by its insidious and metastasizing progeny, namely gaping deficits, unparalleled debt, unequaled malinvestments/misallocations, plummeting productivity growth which new “virus regs” will only worsen, increasingly maligned and eviscerated Main Street property right protections, and now millions of weekly pink slips unlike anything ever seen before. In plain English: with 22m Americans filing for unemployment insurance, or some 12% of the civilian labor force within one month; with record small business closings on the horizon; with supply lines drying up; and with an existential crisis threatening ever more people, the politicians, the bureaucrats, and the above the law “1%” continue to remain lavishly employed and compensated like never before in history.

In all, this threatens the very “system collapse” that Dr. Roberts correctly predicts, in my view, be it socially, politically, financially, or economically (they are all tied at the hip). Unfortunately, doubling down on yet more unsound money-enabled statism/cronyism while restricting commerce, which is what our collective “Corona virus” policy response has been and will likely continue to be, especially given the November election drawing closer, will only expedite and significantly worsen our “day of reckoning.” Why? Because our toxic policy determined by increasingly unconstitutional “authorities” will fail to allow for the very “system clearing reset” (also known as Creative Destruction) to occur that would set the stage for a return to the rule of law, to free market incentives, to property right protections for Main Street makers, to productivity, and thus to “supply side” growth. With a self-enriching, moral hazard-inducing, pork barrel-addicted, fiat money-enabled government refusing to get out of the way, unequaled “double jeopardy” is on offer, which is most worryingly being worsened by soaring approval ratings garnered by totalitarian governors shutting down their states on the one hand, and demanding federal taxpayer rescues on the other hand — “federalism” financed by “the Feds!” Call it a one-two knockout punch of economic shutdowns worsened with yet more counterfeit currency creation and ever more pronounced statism (socialism).

FYI: links were added after the initial publication date in order to provide the reader with articles that expounded on various assertions (money printing, cronyism, infection rate, etc.) that I have made in this post. The same holds true for select content extensions, very much including the closing paragraph, which will hopefully better underpin why we are most unfortunately on “the road to serfdom.” Therefore, this post “stretches” my initial comments made on Greg Hunter’s youtube channel.

The obligatory boilerplate:

This commentary is not intended as investment advice or as an investment recommendation. Past performance is not a guarantee of future results. Price and yield are subject to daily change and as of the specified date. Information provided is solely the opinion of the author at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Information provided has been prepared from sources deemed to be reliable but is not a complete summary or statement of all available data necessary for making an investment decision. Liquid securities can fall in value.

Post #59: A youtube comment section exchange about the “policy response” to the Corona virus

US$: 100.7; Fed’s B/S: $5.8trn;, US 10-yr: 0.59%; S&P 500: 2488; Oil: $28.33; Gold:$ 1,646; Silver: $14.49

Dan here, dkanalytics.com editor. It is Sunday, April 5th, 2020.

Allow me to draw your attention to an April 3rd comment exchange between a youtube subscriber to my channel, Mike, and myself. I will add some food-for-thought links at the bottom of the page that relate to my comments. Sage subscriber Mike wrote the following in the comments section of my youtube micro channel — also “creatively” (not!) called dkanalytics. Here goes:

Mike’s thoughts:

Thanks Dan. I did watch the Jay video and I also discussed this virus with my brother (the immunologist). He advised that the problem with this virus is the speed of transmission which is not fully understood. He mentioned that the advisors to the government are also the same people who would be caught very shorthanded with a medical system unable to cope.

The basic (and belated) idea is to slow the infection rate through social distancing so that hospitals will cope better over a more drawn out period. If not, overwhelming numbers of presenting pneumonia patients will die at a greater rate along with the very many usual IC patients.

It hasn’t been handled well from the outset and vested interests are milking this crisis for all its worth, as you say. South Korea led the way very early in this crisis and provided an excellent model for all the countries that are now suffering. But did anyone else take it seriously from the get go ?. Short answer, no. Very good content. Thanks again.

My thoughts:

Thanks a lot, Mike. And thanks for sharing the invaluable insight gleaned from your immunologist brother. Thanks too for confirming the rapidly spreading nature of the disease. Obviously, this is very difficult to contain — and then to deal with, at the institutional/healthcare level. A German immunologist that I listened to also addressed this aspect. He made two remarks that stuck in my mind. First, people intuitively avoid social gatherings when they are sick or feel sick — especially when influenzas are paying their “seasonal visits.” Second, overwhelmed hospitals in both Italy and Spain are largely the result of creaky infrastructure, lacking equipment, poor planning, very poor hospital sanitation, and (at least in Italy) an older population that is already “compromised” and practices poor hygiene. As a result, Italian hospitals quickly became overwhelmed (happening in NYC as well, for similar reasons and given the “global city” nature of the place), sharply increasing the overall death rate from all kinds of ailments in the process. That same immunologist mentioned that German hospitals, with spare capacity (about a week ago), were taking very ill patients from Italy and Spain, and still had excess capacity. FL governor DeSantis recently issued more decrees to (relatively) modestly reduce freedom of movement, while mentioning that FL hospitals — in aggregate — were in a very good position in terms of beds and ventilators, but that Florida would only take ill Floridian cruise ship passengers while arranging for pickups (I believe with the Coast Guard) of non-resident foreign nationals by their respective country governments.

Separately, I continue to hope that politically incorrect immunologists’ assertion that increasing data about a broad spectrum of people that have been exposed to the Corona virus (a cross cut, if you will) will bear out the fact that the fatality rate of this rapidly spreading virus isn’t too different from other viruses. More data will tell. And, if this is in fact true, i.e., that a lot more people than we know have been exposed to the virus and the vast majority have been able to render it harmless (developed antibodies), then perhaps the rapid transmission rate amongst the broad population has a silver lining via providing “nature’s immunization,” which will hopefully help slow and eventually terminate the damage, from terrible deaths to system overload, that this virus iteration has “unleashed.” As you can gather, this is what I am hanging my hat on, as I lament and fear the “virus response” (the cure may be worse than the disease”).

Lastly, perhaps if the Chinese “authorities” had been more forthcoming, instead of apparently killing doctors that were banging the pots and pans, we might have gotten a faster “heads up,” and could have shielded the most vulnerable members of our population in a “laparoscopic” fashion rather than take out a “kill the economy while socializing and nationalizing it with printed money*” bazooka. Of course, and as you state, information is one thing. How well our bureaucrats would have reacted is obviously another!

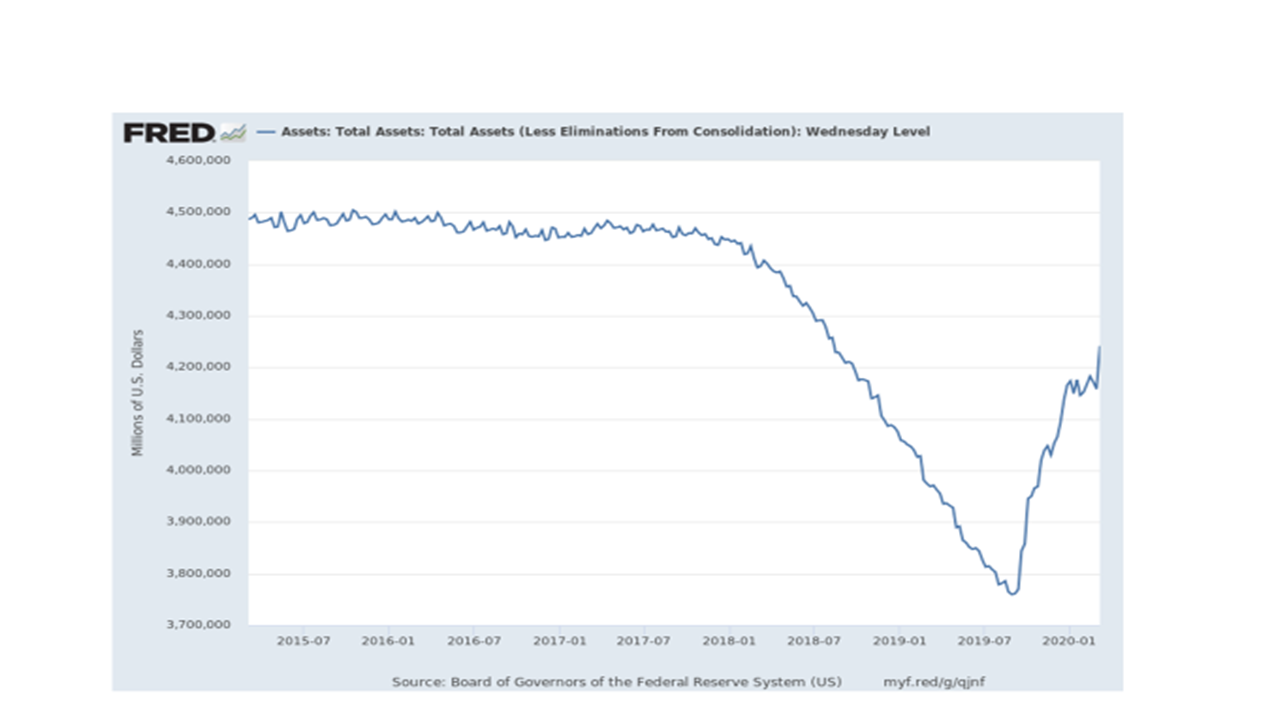

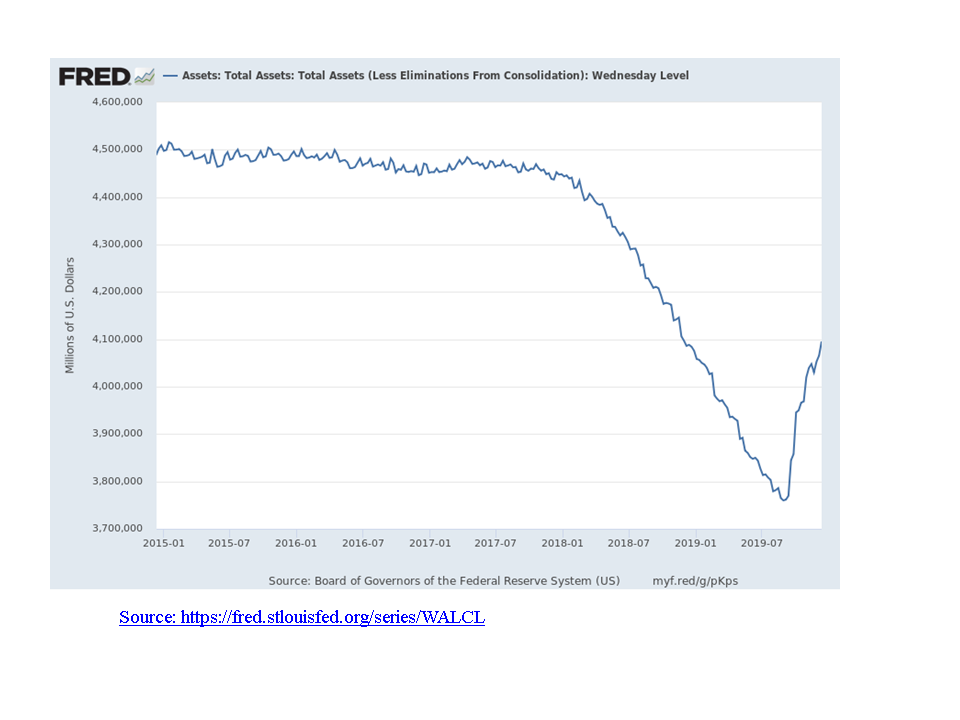

* – That printed money bazooka looks like this (please see far right “vertical trajectory”):

Source: https://fred.stlouisfed.org/series/WALCL

Sincerely, Dan

Some links that you might find of interest related to discussed topic; please note that certain links, towards bottom, have been added after the post’s publishing date because I think are illustrative of our current dilemma:

LITERALLY Shutting Down the World for NOTHING – CV “EXPERT” Anthony Fauci Spills the Beans

Questioning Conventional Wisdom in the COVID-19 Crisis, with Dr. Jay Bhattacharya

Prof. Dr. Stefan Hockertz aktuell zur Corona-Krise

Is the Coronavirus as Deadly as They Say?

Is Our Fight Against Coronavirus Worse Than the Disease?

A fiasco in the making? As the coronavirus pandemic takes hold, we are making decisions without reliable data

CORONAVIRUS: Globalism’s Perfect Storm: https://www.youtube.com/watch?time_continue=1563&v=qG33IKaX_yM&feature=emb_logo

Post publication content on “confirmed cases” below courtesy of the Macro Strategy Partnership in London (April 6th, 2020):

The number of confirmed cases worldwide rose 6.0% on Sunday to 1,274,923, the lowest percentage increase since the 10th March. The number of active cases rose 6.1% on the day to 1,014,333. In absolute terms, the daily increase (number rather than percent) in active cases fell to 58,493 from 83,158. It was the smallest absolute increase for 6 days. It should be noted that the data is revised continually so the numbers may differ slightly from Friday, but the trends are very clear.

????????????????????????????????????????????????????????

The obligatory boilerplate:

This commentary is not intended as investment advice or as an investment recommendation. Past performance is not a guarantee of future results. Price and yield are subject to daily change and as of the specified date. Information provided is solely the opinion of the author at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Information provided has been prepared from sources deemed to be reliable but is not a complete summary or statement of all available data necessary for making an investment decision. Liquid securities can fall in value.

Post #58: Recession Morphing Into Depression: Cure WORSE Than Disease? – Interview with Crush the Street’s Kenneth Ameduri

Post #57: Transcript of March 9th, 2020 video labeled “The quickening”

The quickening March 9, 2020

Trade weighted US$: 116.9; US 10-yr: .56%; S&P 500: 2746; Oil: $31.01; Gold:$ 1,675; Silver: $16.85

The S&P gapped down over 200 points or 7% today at the open and closed at 2746, down 226 points or 7.6%, the steepest one-day drop since 2008. Given the sustained implosion of global stock markets and a historic decline in the oil price, which was down a shuddering 24.9% from Friday’s closing price, I want to jump in with a few observations today prior to reflecting on Corporate Anorexia’s long tail impact on both solvency and growth prospects in a follow-up video or post.

- The price of oil is being pummeled by the demand-culling behavioral fallout, which the Corona virus induced lockdowns, cancelled travel, cancelled events (Geneva) and conventions has sharply exacerbated. There is also a market share war that the Saudis are waging by opening their spigots against America’s high-cost, loss-making shale oil extractors on the one hand and against Russian extractors on the other hand. Given the extensive financing provided by US banks and investors as well as the shale industry’s extensive oil price hedging, this will exert additional earnings and balance pressure on those constituencies that provided the funds and are exposed to the hedges. Yet, only roughly 20% of worldwide oil consumed per year is found, the current oil price rout will eventually prove to be a great purchase opportunity. A “supply story” spiked by unprecedented fiat currency debasement in wings. And a demand story that makes fossil fuels indispensable for leveraged output in industry and agriculture, the resulting sales and earnings, and virtually every product or fixture we look at. A demand story that reflects our hugely dense energy-dependent lifestyle.

- (BTW, America’s shale-based oil/natural gas extractors have been the mainstay of “flyover country” industrial strength/growth for over a decade, sucking in huge amounts of chemicals, truckers, truck fleets, domestically made drilling equipment, and capital. When this loss-making party — the industry couldn’t even generate positive net income when oil was at $100 per barrel — finally ends, the fallout on industrial America as well as on investors will be deep and wide. Plus, the stunning, approximately 7.7m barrel rise in daily US extraction over the past 11 years that it has spawned is set to sharply reverse, which, together with declining legacy field extraction rates, threatens to drive our annual oil replacement ratio even further below 20%, highlighting the “supply” story.)

- Investment grade government bond yields are plummeting to all-time lows. The US 10-year has crumbled with increasing speed from 1.92% yield on December 31st, 2019 to a stunning 0.56% yield today; meanwhile, the spread that junk corporates (BB rated) have to Treasuries is widening sharply, up about 120 BPs to 3% within one week. I had mentioned this spread widening as a canary in the coal mine. Well, that indicator has also failed to be a leading one (just like the stock market), and has become a coincidental or even a lagging indicator, despite the $3.2trn plus bloat in non-financial corporate debt since early 2008 in the US alone and an alleged 20% of all public US companies unable to service debt obligations out of their current, rapidly dropping cash flow, much less earnings …

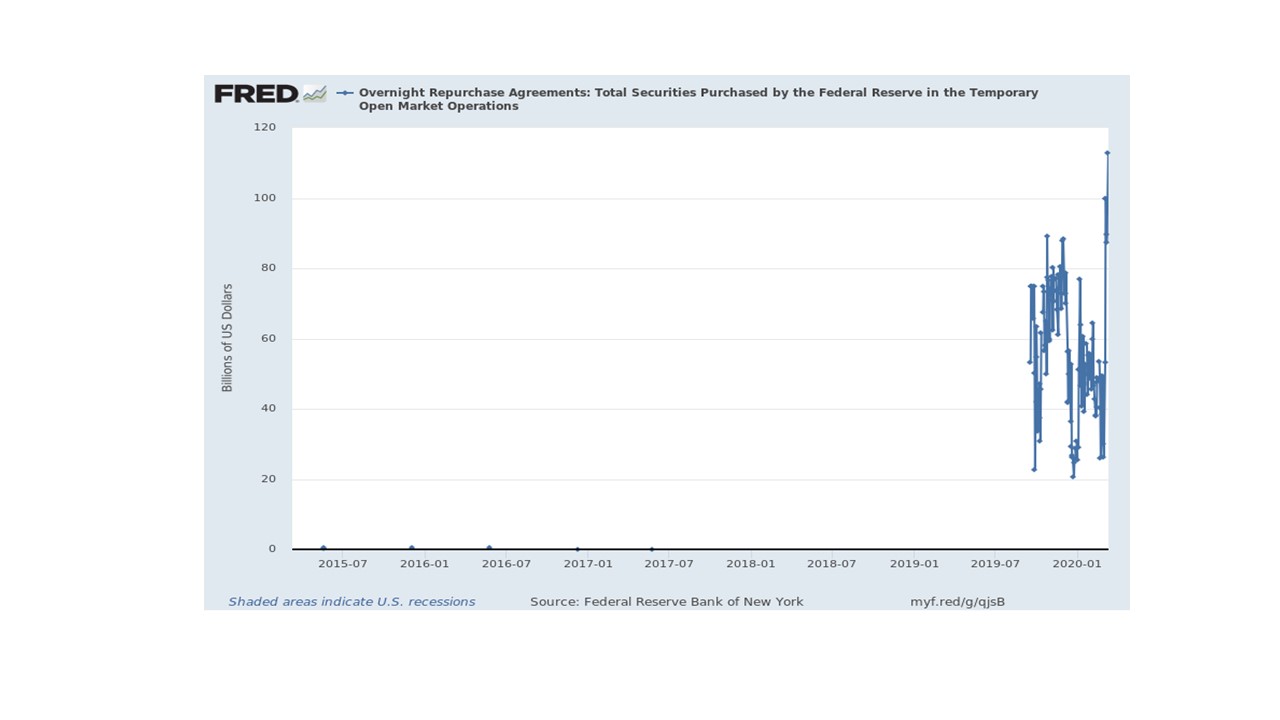

- Meanwhile, the yield curve continues to invert, threatening banks’ liquidity, solvency, and margins, thus the Fed is busy in underpinning the repo market with record purchases and is buying short-term Treasuries like a scalded dog — $60bn p.m. with likely upward revisions in an effort to return to a positive yield curve:

Overnight repo purchases: today (3/9/2020), the Fed purchased $113bn. More bailing out of “casino operations” exposed money center banks in an effort to dictate short-term rates, which shot up to 10% in Repo Land last September.

https://fred.stlouisfed.org/series/RPONTTLD

The Fed’s balance sheet expanded by $83bn in under one week as per 3/6/2020: at a monthly pace, it would amount to over $320bn p.a., blowing away any prior QE by a multiple of 4!

https://fred.stlouisfed.org/series/WALCL

Let me get back to the quickening:

- A US stock market rally until recently fueled by stock buybacks and record margin debt is proving highly susceptible to downward pressure. With buybacks soon to be throttled and margin debt calls soaring, the stock market may remain under substantial pressure, from this dynamic alone.

- With cronyism – big business in bed with big government – ever more rampant and Main Street increasingly locked out of contracts and financing even as it footed larger and larger crony-bailout bills from the S&L bailout to the more recent TARP bailout , small businesses with contracting top lines will likely be even more starved for cash, adding huge pressure to a crumbling economy. Why? Because small businesses are still the backbone of the economy and its where the largest percentage of people in the private sector are employed.

- In short, we may soon face a liquidity crisis on top of a solvency/debt crisis, further pressuring economic activity, which would punish corporate earnings and could precipitate a sustained stock market correction fed by momentum investing in reverse, by algos spitting out a growing frenzy of sell orders, by ETF group think allocations pressuring wide swaths of market sectors now under pressure that rallied so sharply previously, and by technical analysis downside sell confirmations such as 30 – 60 – 120 day moving averages pierced to downside. In short, stock demand may be morphing into sustained share sales — and this is prior to expanding share sales coming from an aging population, which will further pressure P/Es, especially if yield deprivation (ZIRP and NIRP) can be sustained, i.e., investors are forced to liquidate holdings owing to lacking passive income. Arguably, the demographic/aging “P/E compressor” is just getting revved up.

- In the interim, the ongoing flight into perceived safety, such as US Treasuries and other OECD investment grade government bonds from Japan to the Netherlands to Germany to Switzerland, has resulted in absolutely record-breaking low yields/steeper negative yields in record breaking time, as mentioned previously. The increasingly palpable, increasingly widespread investor fear, even panic, as typified by disappearing investment grade yields, should set the stage for another dead cat bounce opportunity in the stock market, which would give investors another chance to lighten up on overvalued stocks bought at dear prices.

- Meanwhile, and this may continue to sound controversial, today’s record-low, (so-called) investment grade government bond yields are also a chance to lighten up on a sector, bonds, that has been in a secular bull market for nearly four decades. For some graphic flavor, consider that yields on the 10- and 30-year Treasuries topped out at 15.8% in September 1981 for the 10-year bond and at 15.2% in September 1981 for the 30-year bond. We’re now below a 1% yield on both bonds – the 30-yr bond is down to an unthinkable, unprecedented 0.94% yield, also virtually “overnight.” The takeaway, and I know if I have thought this at substantially higher yields such as at 2% and 3%, is this: investors should consider reducing exposure to 10- and 30-year Treasuries. Staying on board the 40-year bond bubble brings ever greater duration (extreme interest rate sensitivity), monetary inflation, and solvency risks even as it “imprisons” investors in “yield deprivation land,” which would add insult to injury.

- Investors should also consider taking gains on Frankenstein Finance long-term government bonds featuring negative yields in countries such as Japan, Germany, the Netherlands, and Switzerland. The bond reallocation story here is a simple one: realize capital gains, take the proceeds, and invest same in very short-term investment grade government securities. Such securities sometimes sport higher yields (inverted yield curve), have no duration/interest rate risk, and can’t be bailed in, like your bank deposits can be, namely into “equity stubs” of a failing financial institution. Or, if still possible, just ask to be paid in cash and place your bills/notes in a very safe, accessible place. But do realize that currency in circulation is typically a single-digit percentage of the wider money supply in OECD countries, with the US having a disproportionately high percentage at 9%.

- Also consider dipping your toe into the battered oil/gas sector but focus on plays/companies that have relatively sound balance sheets, relatively low-cost structures, and relatively good reserve status. Given the declining property right protections in OECD countries and much lower valuations and debt encumbrances at the Russian country level and in select Russian oil and gas assets, not to mention a ruble that is still on the floor, don’t get scared out of potentially investing there. You could profit from a great secular supply story that gets another lift from a strengthening ruble that reflects Russia’s much better balance sheet than that of OECD nations.

- Meanwhile, our rapidly deteriorating economic, financial, and political fundamentals prior to the Corona virus impact are now going from bad to worse, yet widespread stock bubbles, and especially bond bubbles, remain.

- It’s beginning to look a lot like this is the real asset valuation reset deal, and that we may only be in the first inning of what will likely prove to be a historic reset which will ultimately massively revalue stocks and bonds to the downside while revaluing real money and scarce, vital, real assets to the upside.

- Once again, I think we will be sailing into a deepening global recession plagued by unprecedented fiat currency creation, unprecedented debt, unprecedented misallocations, and increasingly widespread productivity shortfalls, collectively the difficult progeny of fiat money central banks bent on currency destruction. The Corona virus manifestation serves to speed up and potentially deepen “the quickening.” Needless to say, leading global central banks will continue to respond to their unruly problem children with yet more fiat currency debasement until they have destroyed confidence in counterfeit currencies. Why? Because leading central bankers want to keep their unrivaled power, prestige, privileges – said differently, these bureaucrats want to keep their racket going as long as possible!

- Our predicament and central “banksters” doubling down on more widespread money printing — which could result in a) more expanded stock purchases (beyond the SNB and BOJ “hedge fund portfolios”), b) checks sent to directly to consumers, c) more misallocating, moral hazard bailouts financed by the printing press, and d) other such Keynesian calamities — threaten to bring us a much more virulent version of the 1970s stagflation. Our increasingly displaced free market capitalism, which has been replaced with increasingly entrenched socialism, even cronyism morphing into fascism, is quite the prosperity denuding, productivity pummeling, growth eviscerating, toxic public policy stew. Against this backdrop, expect a much more savage stock and bond repricing, especially given the epic valuation bubbles (especially in OECD nation bonds) we still have juxtaposed against collapsing growth, profits, and solvency ahead of an atypically long and deep recessionary funk. The associated “bust” sentiment shift of investors may prove as difficult to dislodge as the more-than-decade-old bullishness has proven to be. That would result in investors again demanding extremely attractive valuations (low P/Es and high bond yields) in order to invest, especially given the large demographically-based bond and stock sales pressure increasingly in the pipeline.

Concluding thoughts:

Finally, and I know I sound like a broken record, but remember that markets are reversion beyond the mean machines. We spend hardly any time at an average S&P 500 P/E of 16 or an average 10-year Treasury yield at 4.5%. We slice through these valuations on the way up in equity bull markets, and we compress well below them in bear markets, such as with single-digit P/Es (double-digit earnings yields) and double-digit bond yields. Just think back to the late ‘60s, ‘70s, and into the early ‘80s for valuation flavor also known as a 12 – 13-year bear market. After decades of bullish valuations in bonds and stocks — they travel together over time — we are now set for bust valuations that may be with us for a long time, given the extensive damage central banks have done or enabled.

Oh wait, one more thought: if you layer much lower P/Es that will reflect a bond bear market on top of what may be sustainably reduced earnings power/EPS, then you have a value at risk double-whammy: substantially lower EPS and higher discount rates. Not quite a recipe for higher stock NPVs. In fact, quite the stock valuation pressure cooker; combined, I believe stock prices could easily fall between 50% – 75%, possibly more, especially if the ‘70s stagflation on steroids around the corner? I think the odds of that being in our future are higher than 50% that this happens. Caveat Emptor!

I hope you’ve found my “the quickening” observations worthy of your investable assets allocation time!

This is Dan Kurz, DK Analytics, it is March 9th, 2020.

Obligatory boilerplate:

This commentary is not intended as investment advice or as an investment recommendation. Past performance is not a guarantee of future results. Price and yield are subject to daily change and as of the specified date. Information provided is solely the opinion of the author at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Information provided has been prepared from sources deemed to be reliable but is not a complete summary or statement of all available data necessary for making an investment decision. Liquid securities can fall in value.

Post #56: How did the price of silver fare during the stagflationary ’70s — and then some

Post #56: How did the price of silver fare during the stagflationary ’70s — and then some

Trade weighted US$: 90.82; US 10-yr: 1.79%; S&P 500: 3294; Oil: $57.96; Gold:$ 1,550.40; Silver: $17.93

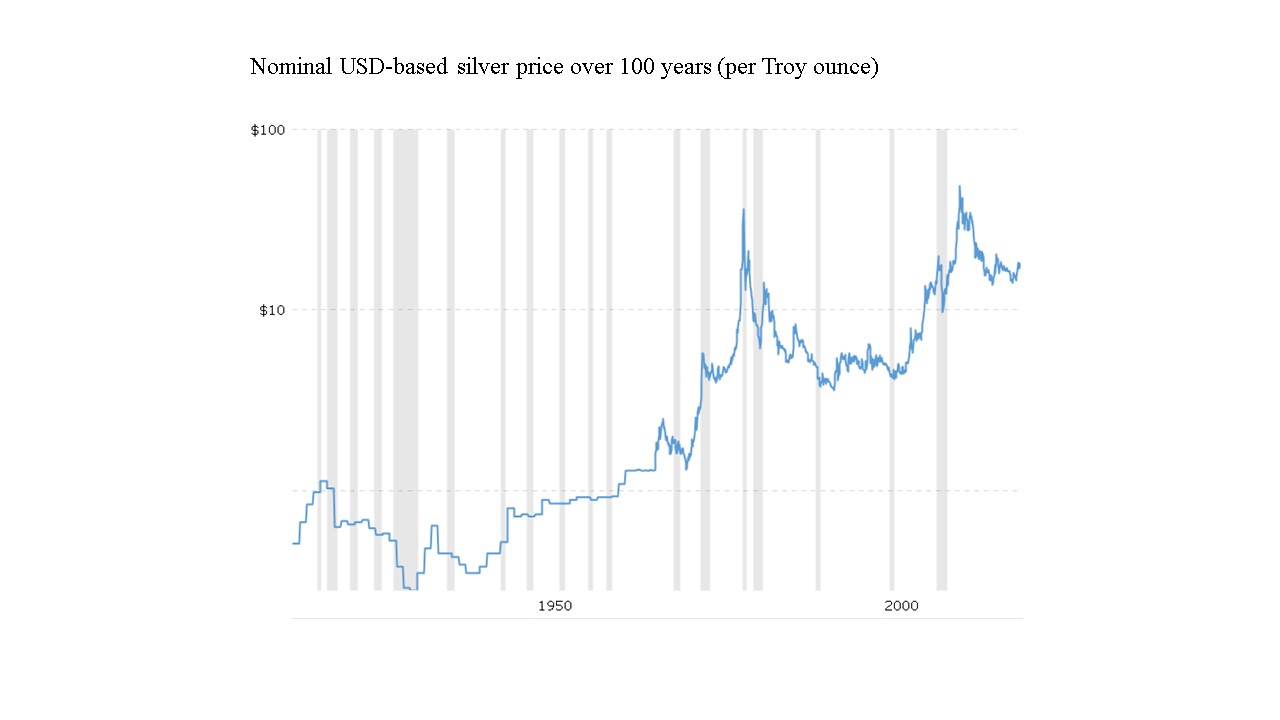

Select financial commentators, pundits, and asset managers have stated that during periods of stagflation — low real GDP growth and high inflation — silver has under-performed gold. Therefore, if an investor believes that stagflation is in our future, that gold will be a better purchasing power protector/enhancer (the latter thanks to sustained precious metals price suppression) than silver. Not so fast, alleged smoking gun backtesting claims notwithstanding.

The stagflationary ’70s — recall that Nixon took the US dollar off the gold standard in August of 1971 — suggest otherwise. From December 1969 to December 1979 (if you were calculating an asset’s upcoming 2020 return, you’d begin with the 2019 closing price and end the year with the 2020 closing price), silver went from $1.83 per Troy ounce to $30.13 per Troy ounce, which constituted a composite nominal return over ten years of 1,546%, or a 16.5-fold rise. See for yourself in the 100-year chart of the US dollar-based silver price. Once you’ve clicked on the link, simply hover over the chart with your cursor, and you will discern the same prices I refer to above. In so doing, make sure you uncheck the inflation-adjusted price selection. This is the chart that you’ll see:

Source: https://www.macrotrends.net/1470/historical-silver-prices-100-year-chart

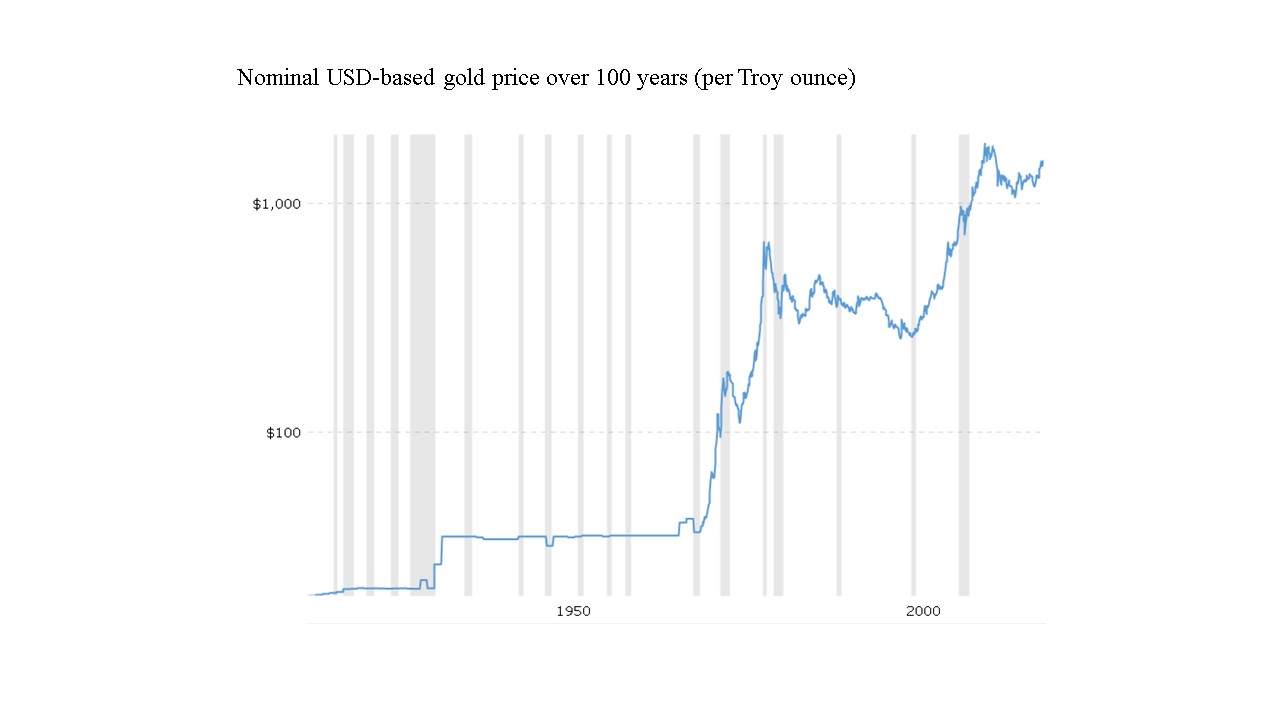

Gold, over the same period (from December 1969 to December 1979), went, in non-inflation-adjusted or in nominal terms, from $41.88 per Troy ounce to $455.92 per Troy ounce. This amounted to a nominal return of 988.6%, or a 10.9-fold rise. To confirm the gold price action, please see for yourself in the 100-year chart of the US dollar-based gold price. Once you’ve clicked on the link, simply hover over chart with your cursor, and you will spot the same prices I refer to above for December 1969 and December 1979. Once again, please uncheck the default inflation-adjusted selection. You’ll see this chart:

Source: https://www.macrotrends.net/1333/historical-gold-prices-100-year-chart

The silver dollar price from December 1969 to December 1979 logged a stout average annual compound return of 32.3% (which comfortably exceeded gold’s 27.0% CAGR over the same time period in the same currency), immense volatility that silver is known for notwithstanding. Granted, silver crashed thereafter, starkly out-legging gold to the downside post January 1980, but the point is how silver does in a stagflationary environment, the inflationary aspect of which then-Fed Chairman Volcker managed to start deflating as he raised the Fed Funds rate from the mid-teens to the high-teens late in 1979 and kept raising it aggressively into 1980, bringing about a Fed Funds rate that crested at an inflation-eviscerating, economy-drubbing 20.74% by December 1980. (Addendum: the fact that the “fiat currency powers of the day” increasingly conspired to shut down the Hunt brothers’ efforts to drive the silver price higher still resulted in even greater white metal volatility while also highlighting just how small the silver market was/is. More on that later.)

Obviously, silver in USD terms does well in stagflationary times, in both absolute and relative terms, i.e., if the ‘70s are any guide. I believe they are. Why? Because post-August 1971, the USD became a 100% fiat (non-precious metals-backed, unconstitutional) currency, which hadn’t happened since the Constitution was ratified on June 21, 1778. The ’70s, assuming they are an unpleasant stagflationary “blast” from the past about to be revisited, are arguably most comparable to today’s counterfeit currency age. That said, current excesses — including peerless debt, America’s unprecedented $10.9trn net debtor status, America’s huge import dependency, and the Fed’s increasingly bloated balance sheet — may well conspire to eclipse both the economic stagnation and inflation (“stagflation”) of the ’70s in convincing terms. At the very least, the ’20s should rival the ’70s in terms of macroeconomic and financial issues. Plus, in stark contrast to even the early ’70s, today’s stocks, bonds (“figure 8”), and real estate are “priced for perfection” bubbles — prior to an inevitable, pronounced EPS compression — despite our increasingly unsustainable, counterproductive economic and financial trajectory. It is this double whammy — negative fundamentals juxtaposed against mania valuations — that suggests a possibly unparalleled asset revaluation (a valuation reset of all assets and currencies relative to gold) draws ever closer; a reset which may well make the ’70s stock, bond, and real estate valuation carnage extending into the early ’80s pale in comparison.

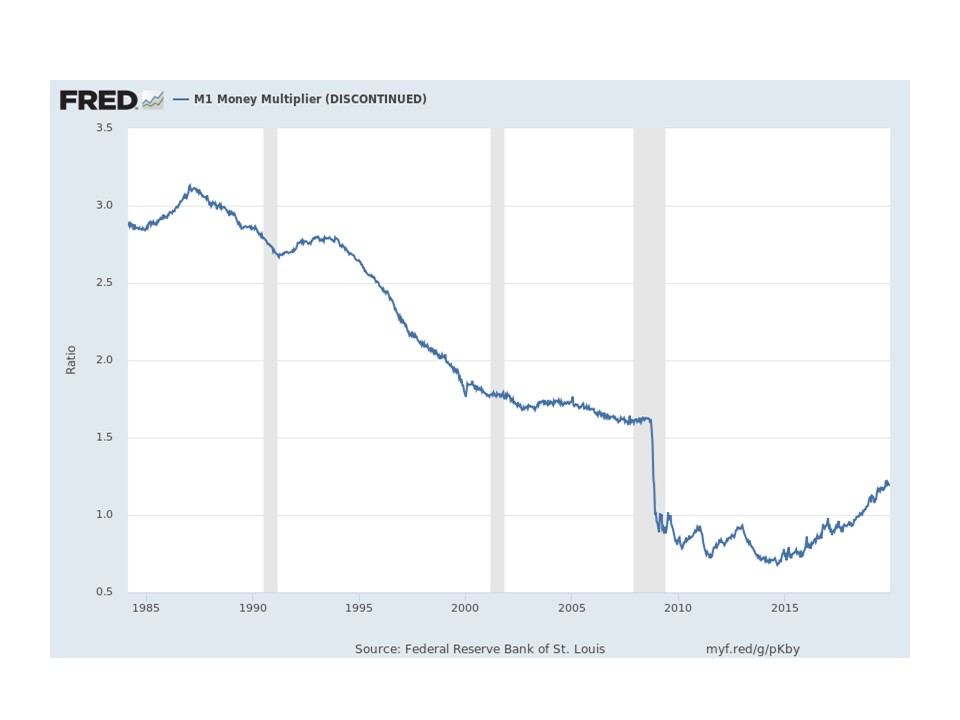

Arguably the only thing more benign than the ’70s as we start the ’20s is producer and consumer goods and services inflation. Yet our understated consumer inflation statistics are substantially falsified. For example, the consumer price index (CPI) is comprised of unrepresentative housing and healthcare cost allocations (too small compared to real world consumer spending share), “steak to hamburger substitution,” and hedonic quality adjustments — all politically motivated, of course. In a nutshell, if consumer inflation was still defined as it was in the ’70s, it would be in the high single-digits. Plus, our increasingly widespread financial repression-enabled misallocations (e.g., deficitary redistributionism of various sorts) are much more threatening to future productivity growth, economic growth, income growth, and price stability than the clouds on the ’70s’ horizon. And “all that” is prior to the monstrous monetary base bloat shifting decidedly from financial assets to real assets in a “crack-up boom,” in which economic participants and investors of all stripes seek to dump fiat currency before it loses (yet more) purchasing power, in the process triggering a self-reinforcing snowball effect. This “buy it now” inflationary bias boosts the money multiplier, which declined into late 2014 and only started to slowly emerge from its decade-old asset bubble stupor as of 2015. For graphic flavor, please see below, and while you do, note that the series has “conveniently” been discontinued by the Fed (perhaps the multiplier was getting “too lively?”): Source: https://fred.stlouisfed.org/series/MULT

Source: https://fred.stlouisfed.org/series/MULT

In a related fashion, perhaps it is not so surprising that consumer and producer inflation rates have also been rising since early 2016?

When combining a reviving money multiplier with a rapidly expanding Fed balance sheet, which is nearly back to record size, or 4.7 times early January 2008’s footprint, monetary inflation begins a migration from asset prices to goods and services prices. If sustained, the money supply (whatever flavor) surges, and monetary inflation (true inflation) can no longer be contained in asset bubbles — especially if foreign creditors “go on strike.” And as the song goes, “we have only just begun” what will likely prove to be a self-reinforcing rise in producer and consumer price inflation, much of it triggered by changing inflationary expectations (in essence from don’t purchase “today” for it will be cheaper “tomorrow” to buy “today” before it costs more “tomorrow”), something which a plummeting dollar would obviously spike materially as regards both the US price landscape and its real economic growth rate. This rings all the more true given how deeply entrenched foreign components have become in goods sold in the US (quite the historical contrast!), whether imported or domestically assembled on the one hand, and given the tapped-out nature of American consumers on the other hand. Said differently: making less yet spending more isn’t sustainable forever, even in America — is it?

For more perspective, let’s briefly revisit the stagflationary ’70s. This was a decade during which consumer price inflation averaged 7.4% p.a. (vs. the “teens”‘ ended in December 2019, a decade during which consumer price inflation averaged 1.7% p.a). Moreover, the ’70s also constituted a decade during which the US “only” ran a net export of goods and services deficit of $206bn, or an average of $20.6bn p.a. (vs. the current annual net export deficit of $653bn, a deficit which is broadly representative of the past 15 years!). This pointed to a ’70s economy that was not materially dependent on foreign-sourced goods, making it less susceptible to swings in the value of the dollar and to external financing costs, despite the issuance of Carter bonds. It was also an economy which, in December 1979, featured only $4.4trn in aggregate debt (vs. $76.4trn today) while America was still a $232bn net creditor nation (vs. today’s $10.9trn net debtor status). This meant that Americans’ collective income in the ’70s wasn’t facing the same interest expense as is currently the case (“back of the envelope:” $4.4trn at approximately 10% back then was $440bn; $76.4trn at about 3% today is $2.3trn). Moreover, the US’s ebbing net creditor position as of December 1979 still nominally bolstered or augmented domestic income courtesy of positive net overseas investment returns. Said stands in contrast to the current predicament, in which “America, Inc.” is increasingly paying interest and sending dividends to overseas investors in order to run deficits and to “buy stuff.” It’s loosely akin to burning furniture to keep warm.

Given America’s outstanding debt, just think of what will happen if average borrowing costs go up by only one percentage point? How does a fat $760bn, or 3.5% of US GDP, in additional interest expense sound just based on today’s aggregate debt outstanding, much less reverting beyond the 4% mean on 10-year Treasuries with a risk premium of at least a percentage point or two for the other domestic borrowers due to those debtors lacking broad taxing power AND a printing press? Reversion beyond the mean always happens, eventually — the benchmark 10-year Treasury yield crested at 15.3% in September of 1981 — given the manic-depressive nature of markets (people).

Now, increasing consumption-related indebtedness in a hard currency (precious metals-backed) world is deflationary simply because you “can’t print money to repay debt or to finance new debt,” meaning consumption declines as debts are amortized, exerting downward pressure on demand, and thus on prices. But the opposite happens in a fiat currency world until confidence in a serially-abused currency, most especially such as the reserve currency dollar, is lost (after which a crack-up boom ensues, which typically sets the stage for an eventual deflationary collapse).

Thus, the less than bizarre takeaway currently on offer in the US: consumer price inflation is virtually predestined to rocket higher. Why? Because with rapidly increasing debt, gaping federal and (US) trade deficits, outsized overseas financing needs, and a dollar which will ultimately reflect domestic and foreign creditors’ continuously increasing value at risk thanks to their financing of a perpetually and materially “negative free cash flow” nation that principally pays its bills via either taking on more debt if it’s cheap enough or via the printing press if it’s not, both accelerated dollar weakness and debasement are all but assured. Foreign creditors will eventually reduce their dollar holdings. Dollars will “come home,” chasing too few domestic goods and services. Long before that, the Fed will “sacrifice” the dollar in even more marked terms than is currently on display in order to protect the solvency and humongous profits of its shareholders, i.e., the member banks that own it — and because of intense political pressure. And speaking of the dollar, consider that even as both US trade deficits and federal deficits have generally soared (both in absolute and in relative to GDP terms) since the late ’70s, the trade-weighted dollar index has also soared, going from 35.89 in December 1979 to 129.36 in December 2019! How does one spell “disconnect?” Haven’t market participants been irrational long enough, Mr. Keynes?

And, once again, stagflation, which got its name during the inflationary recession between 1973 and 1975, not only refers to pronounced consumer price index (CPI) inflation, but it also refers to low or negative real GDP growth. Real US GDP declined from Q2:1973 to Q1:1975 by 2.7%. The consumer price index over the same time period surged at a 10.6% annualized rate. From Q4:1969 to Q4:1979, real US economic growth slowed from 4.4% p.a. in the prior decade to 3.3% p.a. during the ’70s. Back in the day, from a post WWII perspective, 3%-ish annual real growth was rather sedate compared to the 4%-plus norm of the prior two decades, which also featured a consumer price index that was increasing at an average 2% annual rate, a stark contrast to the CPI inflation of the ’70s, when it averaged 7.4% p.a.

In today’s misallocated, expanding government, increasingly deficitary, regulatory compliance ($1.9trn p.a. in America alone, or nearly 10% of US GDP) and US litigation cost insanity, productivity-drooping global economy featuring an aging population and growth-killing financial repression (no incentive to save, stock buybacks over cap ex), re-achieving sustainable 3% real GDP growth in the US or in the OECD world would be akin to the eighth wonder of the world. Yet, to sustain the deeply entrenched bureaucracy (statism), to protect the kleptocracy’s immense power and wealth, and to re-elect redistributionist politicians dealing with high youth unemployment while pronounced pension underfunding increasingly threatens OECD baby boomers’ “golden years,” the printing press(es) will be doubled down on until confidence in fiat currencies turns into flight from them, which is also known as hyperinflation. We are already seeing the initial doubling down unfold in both the US and in the EU — it never stopped in Japan. A case or two in point: just the threat of a lingering or deepening stock market correction (as in Q4:18) or the recent repo “flare-up,” which threatened to upend/trump the Fed’s short-term cost of funding diktat (the Fed Funds rate), are enough for the Fed to take out the proverbial money printing fire hose in order to protect its crony Wall Street owners.

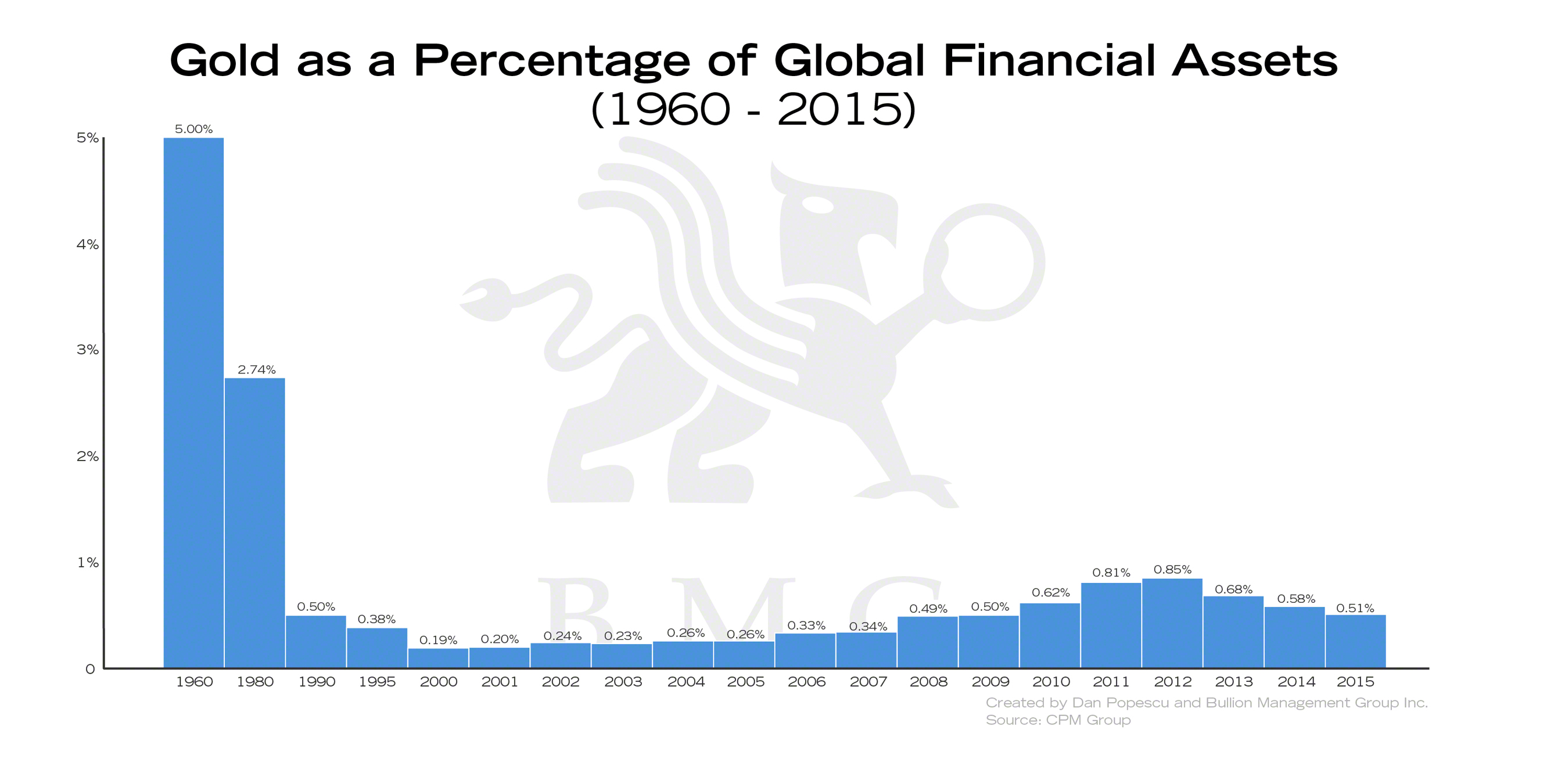

The upshot: the ’70s stagflation, revisited we’re staring at — especially in the US — threatens to make both the ’70s real growth and inflation numbers look good by comparison. Translation: flight into the only true and portable wealth preservation assets/true money over thousands of years, namely scarce gold (about $140bn mined p.a. at the current gold price) and extremely scarce silver (about $15bn mined p.a. at the current silver price), ought to be even more pronounced than was the case in the ’70s as global central banks initiate even more conspicuous, “beggar thy neighbor” currency debasement. This is all the more true when juxtaposed against global investable/financial assets (mainly in bubble valuation bonds and stocks) in the $200trn range featuring approximately 1% exposure to precious metals (virtually all gold), a level that is quite the contrast to the 2.7% exposure in 1980 or 5% exposure in 1960. Just a 0.5% global reallocation to precious metals at current price levels would overwhelm current mining output for approximately six years, meaning that any reallocation would be principally driven by much higher precious metals equilibrium prices. When this sentiment shift comes, it will utterly overwhelm the long-standing, well-known gold and silver price suppression. In fact, that very suppression (effectively, massive naked shorting of both metals) will likely conspire to vault both gold and silver prices even higher, courtesy of “short-covering.”

{kind=link}

Finally, a few more indications as to why silver ought to again outperform gold (in USD terms) as we draw ever closer to 1970s stagflation “on steroids.” The silver-to-gold ratio back in December of 1969 was 23:1; it’s currently nearly 87:1. This suggests that silver has HUGE catch up potential not only because of how silver comes out of the ground relative to gold (it has fallen to 9:1), but because over the course of history it has been Persia’s money, Rome’s money, Great Britain’s money, “the people’s money,” and constitutional money in the US until 1964. Moreover, because silver mining output has lagged silver demand by an average 23% for a decade. Plus, because of the growing and widening industrial/medical use applications for silver. In addition, because of how little above ground silver is actually “salvageable/reclaimable,” economically speaking: somewhere between the 2bn Troy ounce consensus and my much more conservative 16bn Troy ounce guesstimate, or between $36bn and $290bn at today’s silver price, the latter number a mere 3% sliver of reclaimable gold (the vast majority of all of it ever mined). All said, how does one spell additional catalysts underpinning stout silver dollar price outperformance relative to the gold dollar price, which, as I’ve pondered and attempted to rationalize elsewhere, should exceed $10,000 per Troy ounce of gold (p.10) simply given the huge global monetary base expansion that has ALREADY occurred.

Doesn’t sound much like a silver underperformance story ahead, wouldn’t you agree? More likely is a material silver-to-gold outperformance story. And if you find it plausible that gold, prior to even more pronounced money printing (QE) likely in the wings, both domestically and abroad, is currently worth north of $10,000 per Troy ounce on the one hand, and that sooner or later the silver-to-gold ratio (87:1) has to move more closely towards how it currently comes out of the ground (9:1) on the other hand, then silver ought to substantially outleg gold when the dollar price of gold reenters a secular bull market that takes out the July 24th, 2011 $1,838 gold price high. Of historical significance in this regard is the UK silver-to-gold ratio, which fluctuated between 10:1 and 20:1 for some 600 years prior to the advent of silver demonetization in the late 1800s. This was a multi-hundred year era during which an approximate 15:1 silver-to-gold ratio in Pound sterling terms reflected aggregate extraction costs as well as relative demand for the two precious metals. In such a world, if only partly revisited, a multi-hundred dollar silver price per Troy ounce is entirely possible. And do recall, there is no fever like gold fever — except, of course, silver fever!

Greetings,

Dan Kurz, CFA, DK Analytics

FYI: Edits and select link inclusions to buttress post claims continued after publishing date. Post substance remained unchanged.

Obligatory boilerplate:

This commentary is not intended as investment advice or as an investment recommendation. Past performance is not a guarantee of future results. Price and yield are subject to daily change and as of the specified date. Information provided is solely the opinion of the author at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Information provided has been prepared from sources deemed to be reliable but is not a complete summary or statement of all available data necessary for making an investment decision. Liquid securities can fall in value.

Post #55: Is today’s America a democracy, a republic, or something else?

Trade weighted US$: 91.45; US 10-yr: 1.81%; S&P 500: 3239; Oil: $63.25; Gold:$ 1,550; Silver: $18.14

Happy New Year! May 2020 be fulfilling, enriching, and healthy for you and your loved ones! Given where we’re going, I think strong local networks, good handyman skills, and tight-knit families residing in the same geography will become increasingly important. Call it a “blast from the past.”

I recently shared some thoughts on our political situation with an aware and quite knowledgeable subscriber to my youtube micro channel. The lady’s name is Jane. I hope she doesn’t mind me sharing my feedback to some of her comments and one of her links in post form here. Below some of the “back and forth” in chronological order (I hope!) related to a recent video titled “Massive new printing pushing stocks higher still.”

Before I get there, allow me an augmentation by shedding a bit of light on the involved philosophies turned into political actions in my own words. Socialism is heavy-handed government/bureaucratic interference and control over the economy/the factors of production and is, by definition, individual rights and free market corrosive. As such, socialism can hardly be democratic, as unelected bureaucrats largely determine our fate and that of the economy; not much representative government taking place here, which is part and parcel of an indirect democracy, which in the US is manifested in the population-proportional, directly-elected House of Representatives. Thus, democratic socialism is an oxymoron. Socialism’s more aggressive kissing cousins are fascism (as in Hitler’s socialist NAZI party in Germany) and communism (as in Lenin/Stalin in the USSR or Mao Zedong/Zhou Enlai in China). Fascism has been called socialism with a capitalist veneer; I call it crony capitalism on steroids. For a more qualified definition of fascism, click here or see down the page. Communism, or Marxism, has been called socialism with revolutionary fervor in which violent and socially divisive persecution of the bourgeoisie (the property-owning class which employs people) is its “battle cry;” its raison d’être.

One could say that fascists and communists are fighting for control over the same liberty-denuding philosophy put into political action, i.e., socialism. Said differently, a top-down control turf war between one faction, fascism, which doesn’t nationalize, yet very tightly controls — often for militaristic reasons, as in NAZI Germany and I would argue in today’s United States — private property, what constitutes money, and thus the economy, while the even more virulent faction, communism, is not only a command and control economy, but there is no more private property whatsoever. Moreover, communists will not rest until the last remnant of individual freedom and private property have been expunged. The bloodier the methodology to achieve this goal, the better, as “final solutions” are singularly successful in both taking out any (perceived) resistance to complete despotism while sending unmistakable signals of stark intimidation to both the ruled and those helping to rule.

Now to that back and forth on whether America has become a fascist nation, please see below, starting with initial comments/links:

Jane Self:

I am sharing a few links I have read. https://constitution.solari.com/fasab-statement-56-understanding-new-government-financial-accounting-loopholes/

DK ANALYTICS (please note that I only included one of Jane’s links here not to exclude the others, but because I felt it was most topical to the matter being addressed):

Thanks, Jane, this is a highly appropriate link given the fascist government we now have. I am aware of exactly this “statement 56.” In essence, the US government can determine that any request for clarity regarding undocumented, unsupported, or unreconciled accounting, including $21trn in DOD and HUD funding/spending black holes, can no longer be questioned by US citizens because these matters have conveniently been determined to be related to national security risks, thus no transparency nor accountability can be provided by the US government. This is no way to run a representative, constitutional republic (we are not a democracy, Ms. Fitts, we are a republic; please see: https://online.hillsdale.edu/document.doc?id=232 ). Rather, it is fascistic.

Jane Self:

The link you gave is not “found?”

DK ANALYTICS:

Sorry that you’re having trouble with the Hillsdale link to Federalist 10. I just tried it again, and it worked for me. Maybe you have some kind of VPN running that prevents access? Assume you’re good with the other link that defines fascism nicely. Meanwhile, and back on point, let me see if I can give you some of the first page of Madison’s Federalist 10, where he discusses the nature and attributes of democracies and republics:

“Whereas democracy entails direct rule of the people, in a republic the people rule indirectly, through their representatives. A republic can therefore encompass a greater population and geographical area. This difference is decisive in the American experiment, Publius argues, for an expansive republic is able to control the inherent danger of majority faction. November 22, 1787 The Union as a Safeguard Against Domestic Faction and Insurrection Among the numerous advantages promised by a well-constructed Union, none deserves to be more accurately developed than its tendency to break and control the violence of faction. The friend of popular governments never finds himself so much alarmed for their character and fate as when he contemplates their propensity to this dangerous vice. He will not fail, therefore, to set a due value on any plan which, without violating the principles to which he is attached, provides a proper cure for it.

The instability, injustice, and confusion introduced into the public councils have, in truth, been the mortal diseases under which popular governments have everywhere perished, as they continue to be the favorite and fruitful topics from which the adversaries to liberty derive their most specious declamations. The valuable improvements made by the American constitutions on the popular models, both ancient and modern, cannot certainly be too much admired; but it would be an unwarrantable partiality to contend that they have as effectually obviated the danger on this side, as was wished and expected. Complaints are everywhere heard from our most considerate and virtuous citizens, equally the friends of public and private faith and of public and personal liberty, that our governments are too unstable, that the public good is disregarded in the conflicts of rival parties, and that measures are too often decided, not according to the rules of justice and the rights of the minor party, but by the superior force of an interested and overbearing majority. However anxiously we may wish that these complaints had no foundation, the evidence of known facts will not permit us to deny that they are in some degree true. It will be found, indeed, on a candid review …”

Another heads up, Jane, on our sadly fascist government as defined elsewhere: a great telltale sign of our current political disease is manifested by the fact that NO bigwigs EVER get accused of anything (substantial), much less convicted. Central bankers lie regularly and destroy our once solid, constitutionally-mandated currency while they finance growing statism, cronyism, and the resulting illegitimate concentration of wealth; big bank heads representing banks earning untold billions off of post Glass-Steagall moral hazard (the Fed cabal, which they own, has their back) or engaged in market rigging never face charges, much less indictments, for reckless and/or felonious behavior, save for “billion dollar wrist-slap” fines that pale compare to their mind-bending bottom lines reaching into the hundreds of billions of dollars (instead, they and their shareholders get taxpayer or Fed bailouts when things go wrong); big defense contractors that hideously gouge taxpayers with “multi-hundred dollar toilets” are never indicted; and of course our lawless former top-tier politicians and bureaucrats, the Obama, Hillary, Biden, Holder, Comey, and Brennan types, are now working as “connected consultants,” publishing books, penning articles, and doing interviews on fake news channels, which is part and parcel of the cushy revolving door between the administrative state (the deep state) and big business. Once again, how does one spell fascism? How about “like this?”

And let’s not forget how an arguably average American is treated if he happens to be a sailor on a sub sending home a pride-filled picture until Trump pardoned him, or how Tea Party activists were targeted and harassed by Obama’s IRS if they dared to espouse a constitutional perspective in a PAC format (did I mentioned that no involved IRS heads ever got punished, nor lost their cushy pensions?). Or, let’s not forget what happens to Americans that don’t file or can’t pay what effectively amounts to IRS extortion even as illegal alien criminals can’t be touched in sanctuary (lawless) cities and even as illegal aliens are encouraged to get driver’s licenses in “blue states.” Or, lastly, consider what happened to an innocent American in California that was falsely fingered, indicted, and jailed for producing a incendiary video that “triggered Benghazi.” I could go on, but we know what’s going on! You are either part of the ruling elite or a big business chieftain and their hangers-on, and you are above the law, or you’re a non-privileged citizen that increasingly has to fight to recover, against a ruling mob with virtually endless resources, the very constitutional protections that have too often been stripped away courtesy of fiat law, the antithesis of the rule of law/the US Constitution. (Admission: virtually the only difference remaining between today’s fascist US government and full-fledged socialism/communism is the fact that there is still private property.)

An addendum on our fascist government: we not only have an ogopolistic military-industrial complex that Eisenhower long warned about, but we have only six major media companies left (thanks, “BJ” Clinton) that — as we can see — do the leftist bureaucracy’s bidding else risk FCC license suspension; this is how we got fake news. We also have the United States of Goldman Sachs, and a revolving door between the Treasury and Goldman/Wall Street that facilitates unfathomable taxpayer bailouts and Fed assumption of toxic assets; for recent flavor, think of the “repo bailouts.” We also have “K Street,” where corporate lobbyists hugely influence legislation and regulation (where it’s really at, right bureaucrats?) to throw sand in competitive gears, in the process increasing the profits of an ever more oligopolistic private sector (the return on K Street lobbying is absolutely astronomical; how does a composite return of 200:1 or 20,000% sound!). Of course, the involved bought-off legislators (the vast majority on either side of the aisle, which is why I tell my closest friend from childhood that donating to any politician’s campaign is akin to giving a married man money to go to a brothel) can look forward to very lucrative “post office” DC-access/lobbyist careers with those very companies they helped in terms of securing privileged access, contracts, and crony profits. That is, once they stop supporting, as legislators or high-level bureaucrats, corporate welfare at taxpayers’, small companies’, and free market capitalism’s expense and start pursuing their highly remunerative, “post public sector” lobbyist careers. As such, is it any wonder that so-called private sector profits keep getting increasingly concentrated in the very big cap arena that has government access (big business in bed with big government is being taken to the next level). Or, is it any wonder that ten of the twenty riches counties in the US are clustered around Washington, DC? Or that the concentration of wealth is in ever fewer hands and unprecedented in scale? How does one spell fascism? Or how about like this:

“Where socialism sought totalitarian control of a society’s economic processes through direct state operation of the means of production, fascism sought that control indirectly, through domination of nominally private owners. Where socialism nationalized property explicitly, fascism did so implicitly, by requiring owners to use their property in the “national interest”—that is, as the autocratic authority conceived it. (Nevertheless, a few industries were operated by the state.) Where socialism abolished all market relations outright, fascism left the appearance of market relations while planning all economic activities. Where socialism abolished money and prices, fascism controlled the monetary system and set all prices and wages politically. In doing all this, fascism denatured the marketplace. Entrepreneurship was abolished. State ministries, rather than consumers, determined what was produced and under what conditions.”

So much for the youtube comments, observations, and claims. If “all that,” namely our currently fascist state in which two warring factions of socialism keep fighting for the upper hand, doesn’t ring any bells, consider the fact that both parties, at the end of the day, work together to further one or another form of totalitarianism in which politicians and bureaucrats — principally leftists — on either side of the party aisle end up enabling or refusing to act to rein in lawlessness committed at the upper echelons of an increasingly unconstitutional government. To do so — just ask Senator Mitch McConnell or Senator Feinstein — would prove self-destructive to both parties’ immense power, perks, and, most of all, their above the law status. For flavor, consider candidate Trump’s debate pledge that if he gets elected, Hillary will go to jail. Soon after Trump became president, he let the world know that Hillary had suffered enough. Or, dwell on the ludicrous “suicide” of highly criminal Jeffrey Epstein that took place in a maximum security federal prison late last year. It just so happens that Epstein was pals with power brokers on both sides of the aisle, both in and out of government. Current US AG Barr’s dad even hired Epstein as a teacher, which Jane Self kindly first drew to my attention. Clearly, Epstein just had way too much “dirt” on our above the law bigwigs, so if he started to “spill the beans,” the American people would possibly come to understand just how corrupt and criminal their leading politicians, bureaucrats, and cronies are. Can’t have that! Still wonder why he was “suicided?”

If you subscribe to my conviction that the US has, in certain respects, become where fascist Germany and Italy left off in their failed WWII Axis efforts even as the left continues to aggressively attempt to completely tilt the country from fascism into full-blown tyranny, also known as communism, how does one invest for this reality? Think of it as financial repression on steroids. Our decade-long, global financial repression has been very, very effective in terms of driving down interest rates for capricious, rapacious, expansionary, deficitary, Main Street property rights-pummeling, redistributionist, price discovery eviscerating, increasingly non-representative/statist OECD governments across the globe. That same repression has also long encouraged debt-laced, C-Suite-self-serving stock buybacks over cap ex/organic growth via unparalleled low corporate financing costs on the one hand (I call it “Corporate Anorexia”), and the P/E inflation that low interest/discount rates bestow on stock valuations on the other hand.

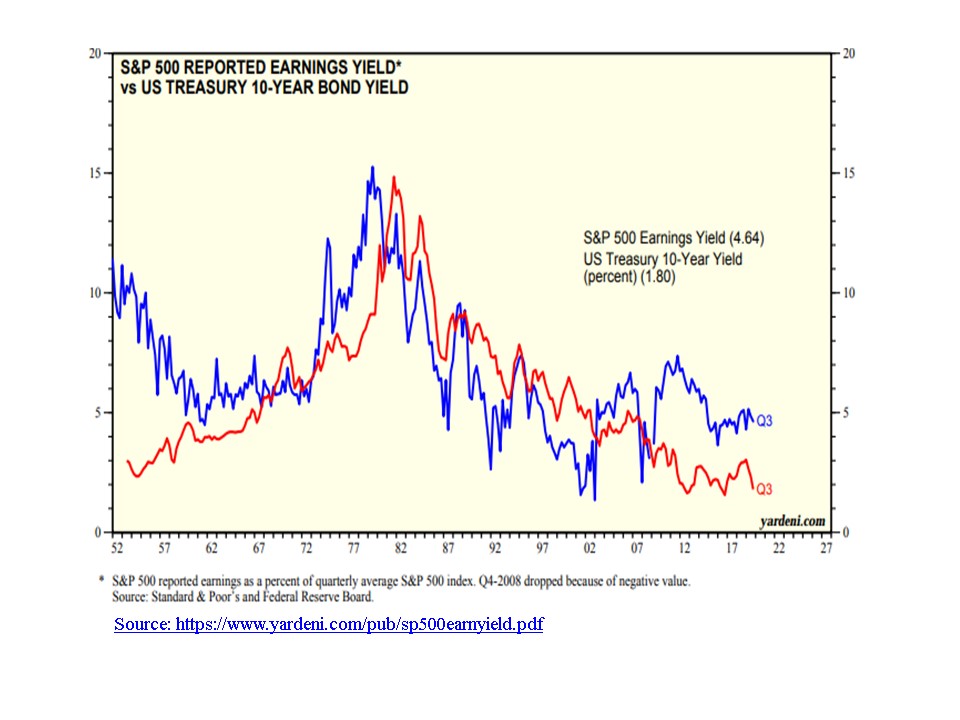

Investors shouldn’t increase exposure to the unsustainable insanity that has worked so well in terms of generating bubble valuations in stocks, bonds, and real estate while simultaneously discouraging savings, investment, and thus productivity and sustainable real GDP growth. While markets have stayed irrational longer than Ben Graham-type thinking investors have been able sustain their clientele, neither the laws of economics nor business cycles have been abolished. The same holds true for markets which, like the humans that define and determine them, display manic-depressive asset valuation tendencies. When our current bubble valuation mania ends, don’t look for valuation reversion to the mean (say 15 P/Es and 4% 10-year Treasury yields in the US). Instead, look for valuation reversion BEYOND the mean, as in single-digit P/Es/double-digit earnings yields and double-digit yields on investment grade bond yields. Look for valuations that will reflect, once again, increasingly entrenched stagflation, the progeny of our long-standing, statist, toxic public policy stew. This is because investors will eventually (again) insist on dramatically widening nominal returns to offset unparalleled and expanding monetary inflation and debt default risks, both of which the printing press “fathered,” and both of which will only get worse until misplaced confidence in the fiat currency status quo crumbles. For a graphic historical illustration of how this “played out” in the stagflationary ’70s, please see, yet again, the excellent Yardini chart below:

Commensurately, investors should reallocate to assets that have been punished by statism on the one hand, and will do well in a stagflationary environment that is a near given going forward thanks to our long-standing, productivity-drubbing misallocations on the other hand. Think of it as the ’70s on steroids aggravated by inconceivably higher debt levels, much bigger governments, incomparably more regulatory compliance costs (estimated at $1.9trn in the US alone), rapidly aging populations, and unparalleled pension under-funding, both the private and public sector varieties. Call it the disgrace of financial repression and dishonest accounting assumptions coming home to roost.

Now, take it one step further, as deficits, debts, under-funding, and declining consumer purchasing power all threaten to become increasingly worrisome and testy. How do statists (our OECD governments) retain control as financial and political stability threaten to crumble? I’d argue that they already have implemented the necessary measures. It’s known as fascism. In the US and elsewhere, including of course Germany in WWII, if all else fails, they take you to war. The US has typically been in non-stop wars of one or another kind for decades. Not only is this a great distraction to avoid closer inspection of what’s wrong at home, but it convinces drone citizens that they must yield more and more of their dwindling circle of liberty — for their own safety, of course, as in the Patriot Act — to the Feds. Same goes elsewhere, be it in the investment business (the disastrous Dodd Frank legislation), in the pharmaceutical industry (the FDA forbidding even patients with a very short life expectancy from getting access to potentially life-extending drugs unapproved by the agency while the cost of getting new approved drugs through the bureaucracy are so stark that all but the biggest pharma companies are pushed aside), in the insurance business (family budget-dominating Obamacare and more), in the energy business (the outrageous, property rights-curdling SCOTUS’s Mass vs. EPA decision, which falsely, incompetently, and destructively determined that coal power-based CO2 emissions threatened the environment; a Europe that has gone green crony energy insane, in the process making power less and less affordable for average citizens; and leftist California, which recently mandated that all new houses must be subsidized by taxpayer-financed solar equipment with incredibly poor ROIs, are all indicative of our global slide into unaffordable, non-24/7, productivity-and-output-diminishing power), in the media business, etc.

In other words, wherever we turn, government is in our face, and crony capitalism/statism has morphed into more aggressive fascism, which is in a fight against the communist faction of socialism to determine our future (interestingly and disturbingly, both factions seek to project national/military power on to other nations). While we are likely off the rails politically and socially — and we’re collectively way too indoctrinated/uneducated/still too comfortable to fight for the declining scraps of liberty remaining — the misallocations, mispricings, bubbles, and unmatched debt edifices that our toxic, increasingly despotic public policy stew has brought suggests that we have to reallocate our investable assets quite dramatically to reduce capital impairment risk and to optimize strategic return potential. I’m referring to embracing the very assets that will give us a chance of arresting our economic/output decline. Select dense energy assets and the related infrastructure, from nuclear to all fossil fuels (especially coal), immediately come to mind, for leveraged output (our economy) depends upon these very assets being properly deployed. Translation: even affordable energy-destroying leftists and crony capitalists (they are in bed with each other) cannot afford to sustain a policy which will incessantly collapse our way of life or our GDP per capita, so invest in attractively-valued dense energy assets before they are again “politically correct” due to economic necessity. The gathering global weakness may provide for an even more attractive entry point.

Meanwhile, shield or reallocate your investable assets (e.g., your overvalued stocks and bonds purchased at rich valuations) from the unavoidable doubling down on financial repression — as recently commenced in unparalleled terms by the Fed — which threatens to increasingly strip away what remains of our fiat currencies’ dwindling purchasing power while at some ever-closer point threatening to collapse the misplaced confidence in our increasingly dysfunctional and perpetually less sustainable fiat currency system. Protect your “value-at-risk,” investable assets from the upcoming, beyond-the-mean valuation reset. And, because we all need to eat, select assets in the long-ailing ag sector should also prove good diversifiers while offering solid strategic return prospects.

Fascists will increasingly covet control over vital real assets (and real money) if they are to have any chance of sustaining their redistributionist, self-enriching, expanding, command and control economic/political governing system, i.e., avoid either a revolution or an economic/financial collapse, which would likely cost them and their hangers-on their lives while possibly opening the door to socialism’s even uglier faction, Marxism. You have the chance today to pick up various real assets (commodities and the related infrastructure) that have either been panned or simply sold as the madness of crowds and momentum investment strategies (and yes, algos, too) have people continuing to overpay for bonds, for stocks, and even for (yet more) fake money!

Thus, if you can’t beat ’em, at least lead ’em :-)! And if the commies win, everything is lost anyhow, but maybe you’ll be able to use your physical gold and silver stored outside of the banking system. If you live in the US, get some “junk silver” so that you can a) barter better for scarce food and other necessities that will be in short supply thanks both to lingering misallocations and to an at least transitory freezing-up of the credit system upon which everything is based, and b) be better positioned to buy off a Marxist government goon when “push comes to shove.” Gotta have a “Back in the USSR” game plan too, right?

Sincerely,

Dan Kurz, CFA, DK Analytics

FYI: Edits and select link inclusions continued after publishing date. Post substance remained unchanged.

The obligatory boilerplate:

This commentary is not intended as investment advice or as an investment recommendation. Past performance is not a guarantee of future results. Price and yield are subject to daily change and as of the specified date. Information provided is solely the opinion of the author at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Information provided has been prepared from sources deemed to be reliable but is not a complete summary or statement of all available data necessary for making an investment decision. Liquid securities can fall in value.

Post #54: Transcript of December 19th, 2019 video labelled “massive new money printing pushing stocks higher still”

Transcript of DK Analytics December 19th, 2019 video

Topic: massive new money printing pushing stocks higher still

Trade weighted US$: 91.76; US 10-yr: 1.93%; S&P 500: 3,198; Oil: $61.00; Gold:$ 1,476; Silver: $17.07

One housekeeping issue: I’ve spent way too many off-hours trying to make sure I don’t lose my site! My extremely talented webmaster out of Bratislava is retiring at year’s end and I had to find “Plan B” (with his help) while also trying to find a substantially cheaper hosting solution with bigdaddy. I managed to get all the ducks to line up, taking another 70%-ish chunk out of my annual out-of-pocket related to the site, so I may publish (some) of my transcripts. This is the “pilot version,” for better or worse. And I don’t know if “that plane will ever fly again.” Just saying.

Prior to wading into the topic at hand, allow me a few political remarks as regards the impeachment hoax: