Post #50 is a DK Analytics video on financial and economic challenges juxtaposed against asset bubbles

Post #49 is a DK Analytics video on politics juxtaposed against asset bubbles

Post #48: Lior Gantz of Wealth Research Group interviews your author on a broad range of political, financial, and economic matters

Post #47: With rising interest rates, if you must buy, purchase “value” vs. “growth” stocks — AND THEN SOME

DK Analytics, Post #47: With rising interest rates, if you must buy, purchase “value” vs. “growth” stocks — AND THEN SOME 9/20/2018

Trade weighted US$: 90.03; US 10-yr: 3.08%; S&P 500: 2,908; Oil: $71.66; Gold: $1,212; Silver: $14.34

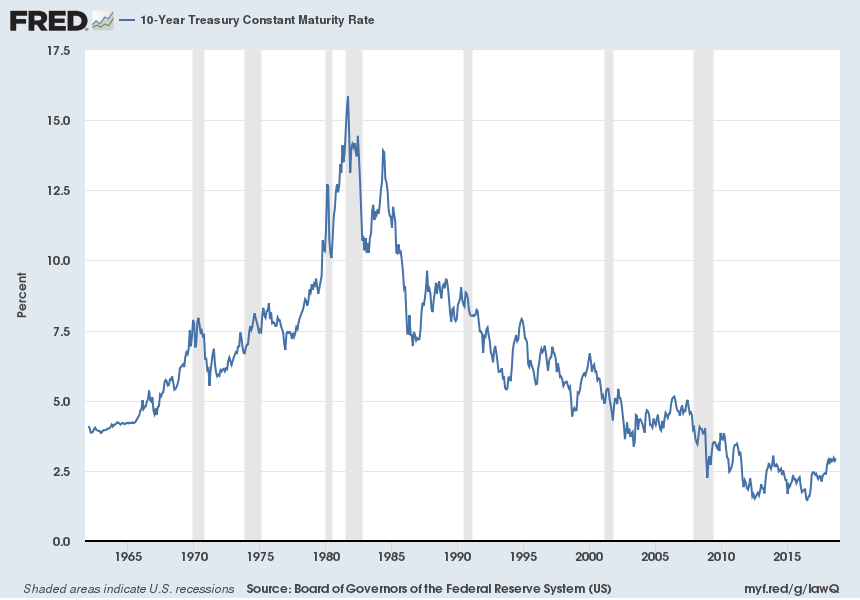

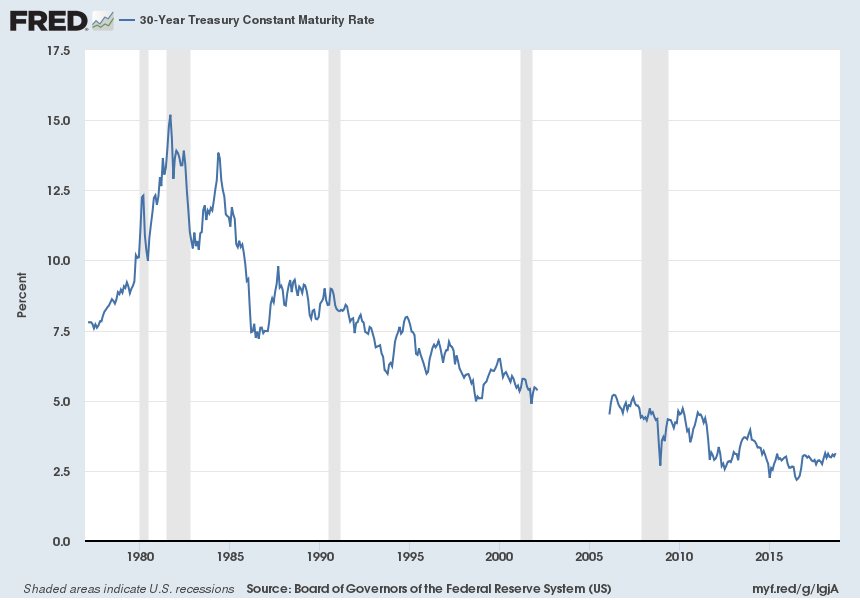

A historical interest rate perspective — the US & the world have never been so indebted in both relative to GDP and in absolute terms, yet look at our interest rates:

Source: https://fred.stlouisfed.org/series/DGS10

Source: https://fred.stlouisfed.org/series/DGS30

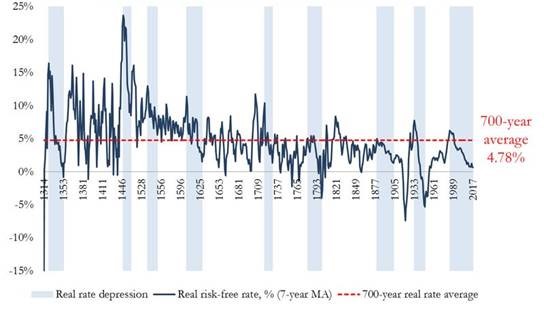

The real risk-free rate since 1311 (translation: risk-free, inflation-adjusted borrowing cost or interest rate)

Source: www.bloomberg.com/news/articles/2017-11-07/centuries-of-data-forewarn-of-rapid-reversal-from-low-interest-rates. For flavor of what higher discount rates would do to the current S&P 500 valuations, click here.

First, after a decade of global financial repression now reversing, US stocks (and part of the world’s) are pricey prior to an overdue recession that should pummel EPS:

S&P 500 P/E based on trailing 12-month GAAP EPS

Source: http://www.multpl.com/ Mean P/E: 15.73; Median P/E: 14.73; Min P/E: 5.31 (Dec 1917); Max P/E: 123.73 (May 2009)

In terms of the 25 P/E multiple, consider that S&P 500 EPS are being legislatively “juiced” (lower tax receipts amidst record and growing federal government spending) into very transitory double-digit growth. Contrast this with from otherwise very pedestrian, low single-digit GAAP-based EPS growth between 2006 and 2017 (p. 2).

In particular, that “juice” is coming from a pronounced one-time reduction in the combined corporate tax rate (when considering federal and state levies, from nearly 40% to 25%), from massive profit repatriation under a lower repatriation tax (in the main, 15.5% vs. 35%), and from the ensuing record, possibly $1trn plus, repatriation-fueled stock buybacks. Upshot: 2018 S&P 500 EPS, which are tabulating stout 18% year-over-year growth through Q2:2018, would be much lower — and the S&P 500 P/E would be much higher — were it not for these unsustainable (one-time) developments.

This is thrown into sharp relief when examining the lackluster average EPS growth of 2.8% p.a. between 2006 and 2017. Punk average GAAP (“true”) EPS expansion has long lacked stout organic (top-line) growth, which is unsurprising for nominal annualized EPS growth cannot consistently outstrip nominal annual GDP growth (slide 3), an “econ 101” given. What is more embarrassing, and also frankly foreboding, is that despite unprecedented a) debt-financed share buybacks with “cheap money” that are looking eerily like “public LBOs,” b) domestic personnel reductions, and c) stagnant nominal cap ex and the ensuing moderating depreciation expense (in a nutshell, “corporate anorexia“), 2.8% EPS compounding was the best that a massively overpaid, stripped of parallel strategic interests “C-Suite” could “conjure up” from 2006 to 2017. (And yes, Virginia, we do have to deal with EPS eviscerating recessions, which haven’t been render obsolete, and with huge restructuring charges in continuing business lines, when looking at longer-term EPS compounding.)

The financial engineering-driven (versus real engineering-paced), anorexic, American C-Suite legacy threatens to magnify EPS compression prospects during the next recession from both corporate debt encumbrance and from weak product portfolio vigor perspectives. A run-of-the-mill, 40% -50% EPS reduction, magnified by the ephemeral tax rate reduction and repatriation-driven “shooting star” EPS surge we’re witnessing, might be substantially exceeded to the downside, and stock buybacks at bubble levels will invariably (again) be followed by EPS diluting secondary stock offerings at “bust” stock prices, adding insult to thinning earnings slice injury.

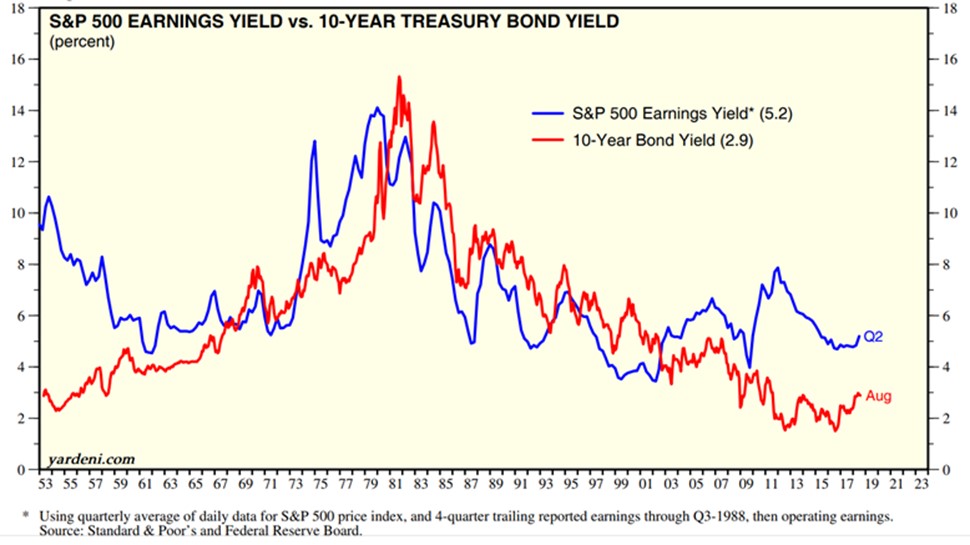

Second, as bond and stock valuations are tied at the hip, rising rates have a similar impact — “bonds and stocks travel together:”

- An increase in the return sought will cause a reduction in the NPV of the benchmark bond (the 10-year Treasury). This is expressed as a rising bond yield and a falling bond price.

- The same holds true for stock valuations/NPVs. When the discount rate (benchmark interest rate plus risk premium) rises, P/Es and stock prices (S&P 500) fall, and the “E/P,” or “earnings yield,” rises.

- Thus earnings yields and bond yields move in tandem:

Source: www.yardeni.com/pub/sp500trailpe.pdf

Please note: if yardeni.com had continued to use appropriate, GAAP-based S&P 500 EPS, instead of bloated/devoid of recurring restructuring charges EPS as of Q3:1988, the mid-September 2018 four-quarter trailing E/P — or earnings yield — of the S&P 500 would be 4.0%, not 5.2%, as stated in the above chart. Looked at another way, investors should be seeing a S&P 500 P/E of 25.2, not 19.3, as a 5.2% E/P implies. And, BTW, all those analysts claiming that recurring restructuring charges (delayed, typically massive expense recognition in continuing business lines also known as “big bath accounting”) can be “ignored” when examining EPS also eagerly tout the higher ROEs achieved thanks to the charges-based equity hits, which obviously magnify future returns on equity! How does one spell “hypocritical” or “disingenuous?” Fortunately, the market can see through some of this, which is why banks and other financial entities prone to large periodic loan or asset write-downs are typically awarded only niggardly P/E valuations.

Beyond understated P/Es and overstated earnings yields, and of arguably useful historical valuation insight given a more virulent form of stagflation (’70s on steroids) that we are steering toward, note that approximately a year prior to the height of the bond market collapse in September of 1981 (the 10-year Treasury’s yield reached 15.2%), the S&P E/P (earnings yield) topped out at a staggering 14%! A S&P 500 E/P of 14 is the equivalent of a P/E of 7.1, a mere 28% of today’s S&P 500 P/E of 25.2. Such a valuation, which I strongly believe is a preview of coming attractions given our political (cratering trust/confidence possibly dead ahead given widespread lawlessness by those controlling the levers of power being exposed), financial (unparalleled global QE, financial repression-enabled debt mountains, and $21trn in unaccounted and unappropriated US government spending), and economic (faltering productivity and rising inflation) “landscape,” will bestow upon equity investors a “generational” buying opportunity.

Caveat: the upcoming equity bear market may well be of a very protracted nature. Nevertheless, outsized returns are made “in the buying,” meaning purchasing select “survivor,” big cap, crony, and/or vital resource stocks (in essence, S&P 500 type shares) featuring single-digit P/Es, double-digit dividend yields, and relatively robust odds that dividend payments can a) be maintained and b) be sustained at current levels, or at least at a substantial fraction (say over 50%) of current levels. This kind of “late ’70s/early ’80s” buying opportunity, when stocks were panned, will be revisited, we believe sooner rather than later.

Third, if you absolutely must buy (we’d wait for widespread bargains), lower P/E value stocks are less susceptible to rising rates than high P/E growth stocks:

During periods of rising interest rates (and let’s not forget that we have reversion beyond the mean, not reversion to the mean!), especially from historically very low levels such as today, investors, to the extent that they: a) have to remain invested in stocks and/or b) have “recent vintage/expensive” exposure to a very overvalued stock market, ought to shift equity exposure into value (lower normalized P/E) stocks from growth (high normalized P/E) stocks. Very importantly, investors in Blue Chips that offer high or very high dividend yields thanks to low historical acquisition costs (low split-adjusted stock prices), or in established growth stocks with low P/Es thanks to low comparative purchase prices that date back a decade or decades ago, should stay put! You already have what others are waiting for, so don’t sell; you wouldn’t sell a delightful, spacious home that you purchased for $38K in leafy, beautiful Niskayuna, NY (where I grew up) just because similar houses are fetching $250K – $300K, because you have already locked in a low cost base, save for “criminal,” perpetually rising (way beyond inflation) property taxes, which would admittedly dilute the validity of this comparison, but not the big picture point.

In a few sentences, and a bit oversimplified but arguably a good starting point for your own analysis for those requiring “perennial equity exposure,” part with FAANG stocks with a current average P/E exceeding 100 and examine the few relatively attractively valued, relatively low P/E names still out there for possible purchase (you’ll need patience, and most will typically go lower after you’ve taken your initial position, so if fundamentals unfold constructively, “dollar average down”). Given the likely economic, financial, and wrenching political/geopolitical storm that we are stepping ever more deeply into, focus on cash flow-stout big caps in out-of-favor industries with strong K-Street ties that have gotten slammed, and hopefully for the wrong reasons, at least strategically speaking. The reasons for this are straightforward:

- The NPV (net present value) or the market cap of lower P/E stocks is less susceptible to compression thanks to the fact that current or near future EPS are high relative to the stock price.

- The opposite is true with growth stocks featuring puny current earnings power compared to the stock price (high P/Es). Here, investors are betting on very significant future EPS growth.

- When investors discount back a “growth stock” EPS bonanza that will lead to a more reasonable P/E years down the road, it’s not too different from valuing a very low-yielding 10-year Treasury, a 30-year Treasury, or even a 15-year zero coupon bond. Reason: something called “duration,” which is the weighted average term to maturity of the cash flows. In the vernacular: the further out beefy EPS residuals are, the more susceptible the stock price (the NPV) is to shifts in the discount rate — an interest rate plus a risk premium (shareholders’ bottom line is known to dip into the red while bondholders get paid in full short of bankruptcy reorgs, thus the risk premium).

- A great rule of thumb: purchase growth stocks (long-duration, high P/E, huge multiple of book value equities) when inflation and interest rates are high, and sell them when they are low (as in now). Contrarily, buy value stocks (low P/E and low price/book ratio equities) when inflation and interest rates bottom out (as appears to be the case today) and sell them when inflation is surging, and interest rates are heading higher).

Motley Fool recently highlighted “bludgeoned” value names, courtesy of their valuation screens, which spat out AT&T, Horizon Pharma, and “Mickey Mouse.” T & DIS trade for a whopping 40% discount — or a P/E of 15 — to the current S&P 500 multiple. Such equities are great places to begin due diligence efforts for qualified investors, who also require at least a modicum of diversification (don’t just buy one!).

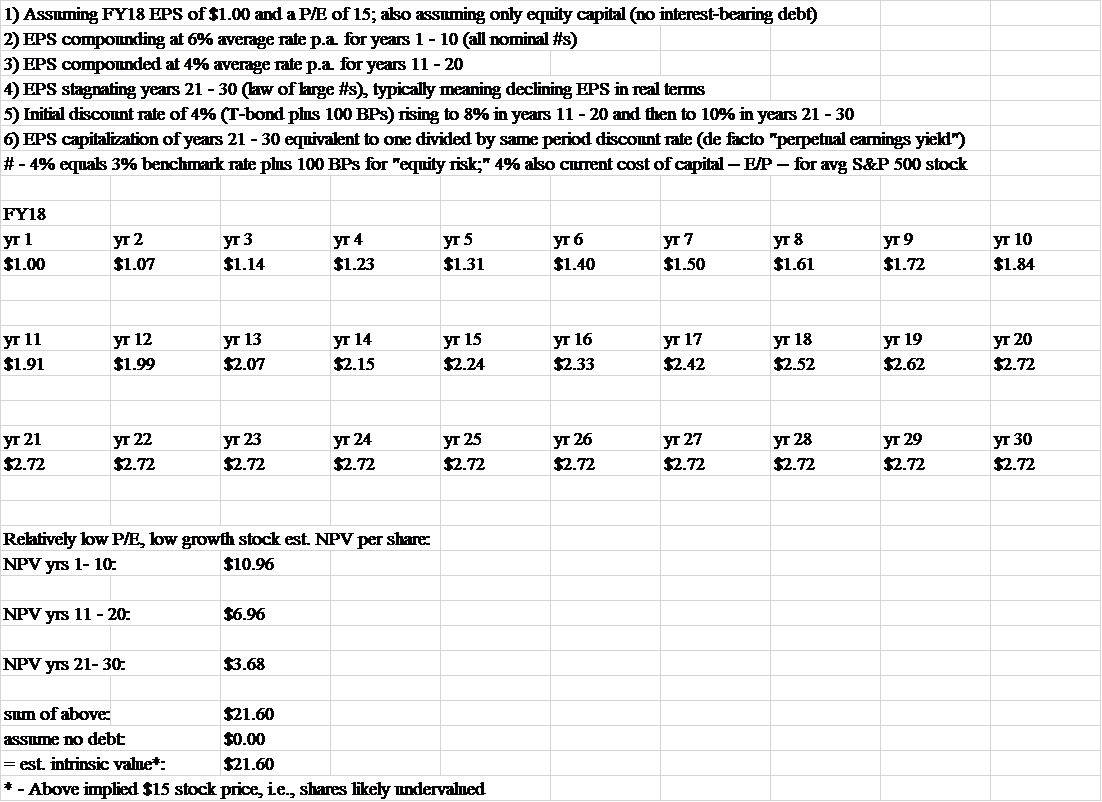

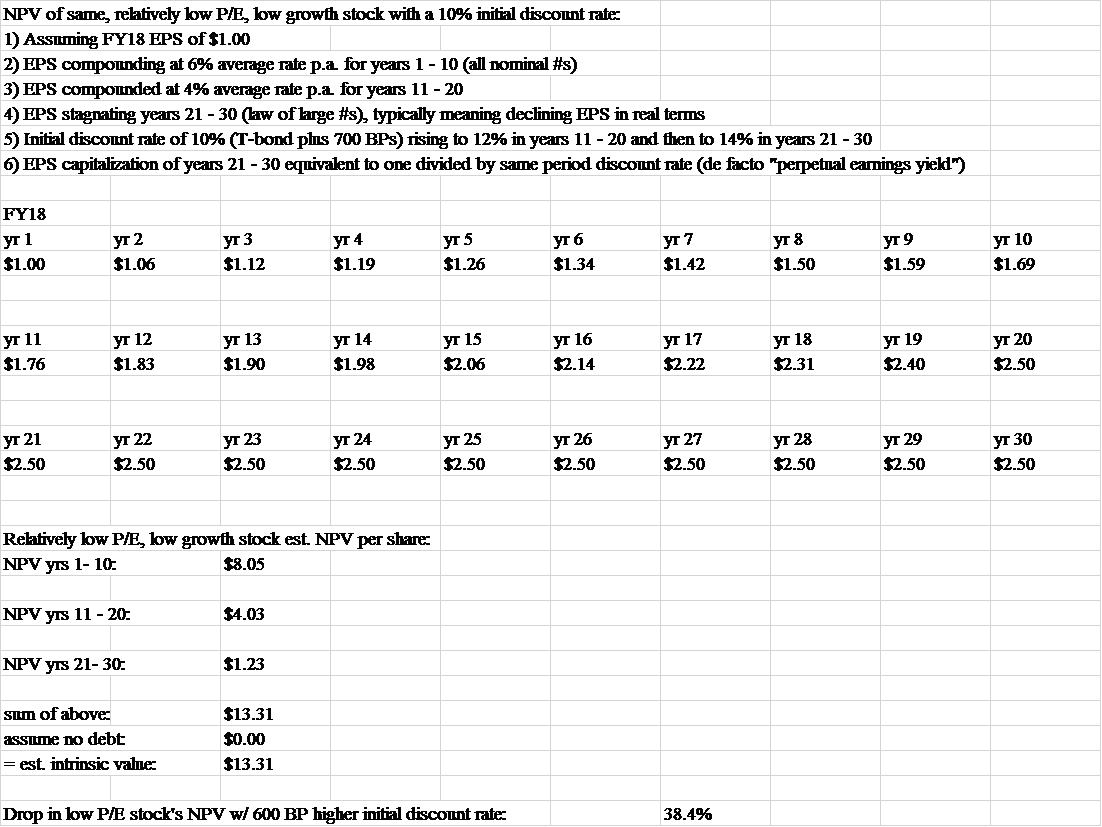

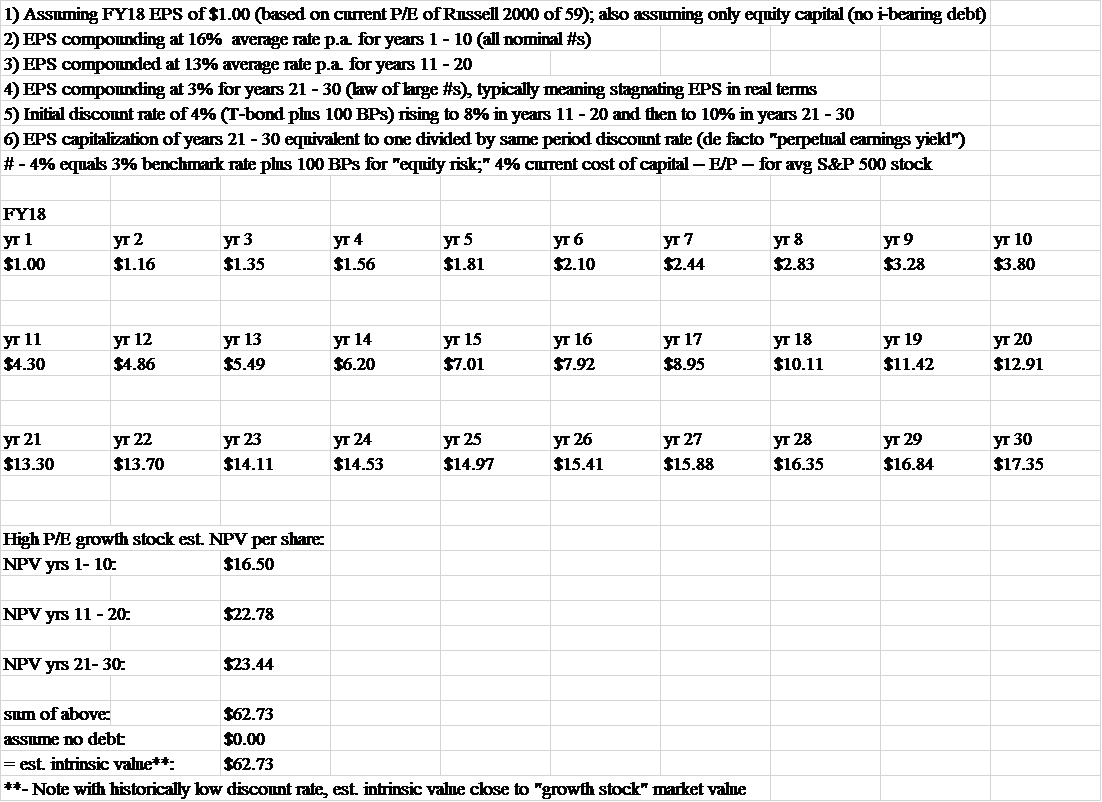

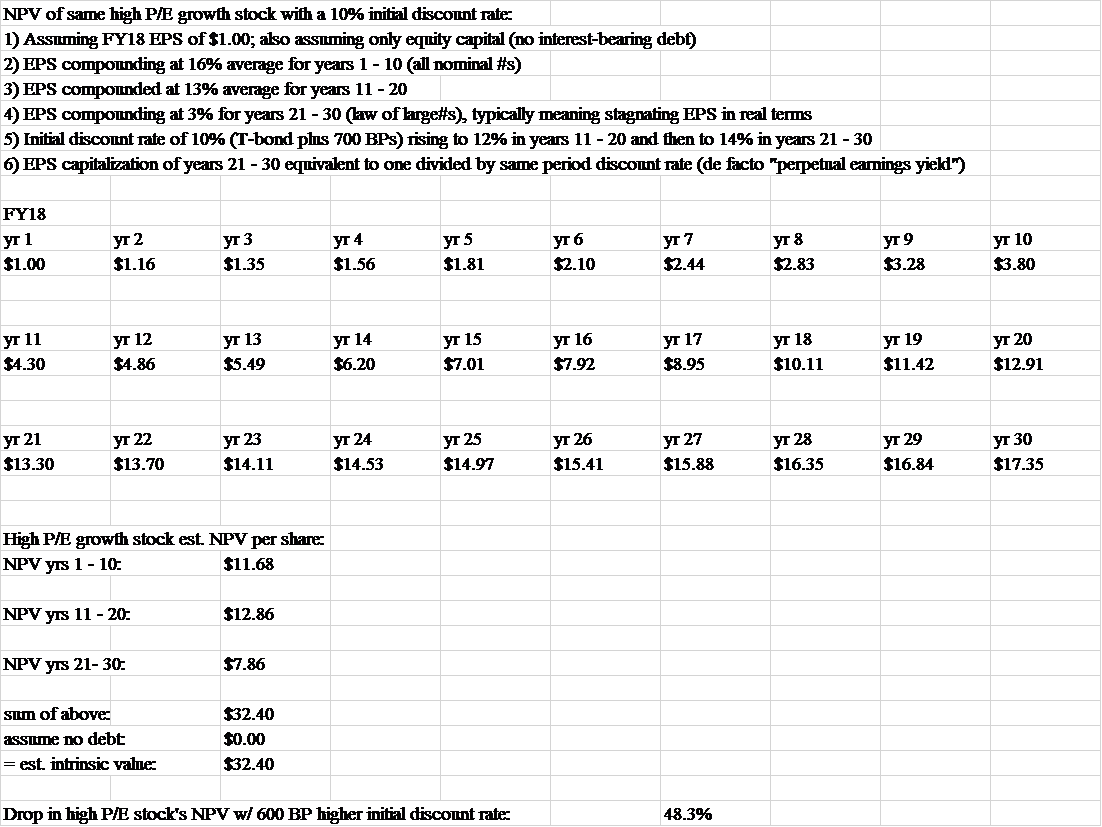

With a few keystrokes devoted to a cursory glance at potential “value names,” let me now take a stab at the NPV impact from rising discount rates (benchmark interest rates plus a risk premium for losses and total loss of capital risks) on a value stock and on a growth stock. The point: to give readers a top-down glimpse into value and growth stock valuations (NPVs, or stock prices) during a secular bond bear market. Based on history, bond bear markets (rising yields) can extend for decades. Note that our current bond bull market is 37 years old.

First the “hit” from higher discount rates to a hopefully somewhat representative value stock (in today’s nosebleed valuation stock market). Below that, the same rising discount rate math “hit” on a hopefully somewhat representative growth stock in the same bubble valuation market. Clearly, nominal EPS growth expectations can be altered with considerable NPV effect. That said, I’ve tried to use at least somewhat realistic EPS compounding assumptions on the value and “established” growth stock fronts over a span of three decades (more details on this in the calculations below as well as in the closing remarks).

The value stock’s price compression in a pronounced bond bear market that has the discount rate going from 4% (30-year Treasury yield plus 100 BPs) to 10% (note that the 30-year Treasury reached 15.2% in September 1981) results in a 38% stock price (NPV/estimated intrinsic value) decline. On the growth stock front, the same discount rate dynamic pushes the stock price’s estimated intrinsic value/NPV down by 48%. I have not tried to capture the reduced economic growth much higher interest rates in a highly indebted economy would cause, but I have called this out in post #42. Suffice it to say that lower shareholder EPS growth would be likely in an environment where new creditors would experience nominal (and ultimately real) yield deprivation relief, i.e., some version of the “1981 stagflation protestation pinnacle, revisited.” And this is prior to any potentially metastasizing trade war, which would have profound inflationary (QE responses) and recessionary — or at least stagflationary — implications.

The resulting NPV calculations are solely efforts to give a sense of the magnitude of stock price compressions from sharply rising discount rates for value and growth stocks. This “top-down” exercise incorporates the impact of stoutly rising — but not historically unprecedented (especially when considering much, much lower US and global public indebtedness in the early ’80s) — interest rates on stock prices in NPV terms. In so doing, the discount rate increase assumption is beyond that was used in an earlier piece on this topic (post #25), which dealt with the S&P 500 Index. The reason: individual stocks obviously carry much higher risks than the S&P 500 as a whole from a host of perspectives. The calculations:

| NPV of relatively low P/E, low growth (value) stock currently trading at $15 with a 4% initial discount rate#: |

| NPV of high P/E growth stock with a current “Russell 2000” 59 P/E or $59 valuation with a 4% initial discount rate#: |

Source: author calculations using Excel financial functions combined with author EPS growth and interest rate/discount rate assumptions

The bigger point, revisited — and expanded:

The bigger point, as addressed both above and with considerable detail in post #25, is that rising interest rates — and the discount rates on which they are based — will punish both bond and stock valuations as they are both discounting mechanisms. This is equally true for most other assets, including mortgage-encumbered real estate and leases of all virtually all sorts. Discount rates, or benchmark rates with shareholder premiums on top, could fatten substantially beyond benchmark rate increases. We haven’t dialed this in; we have, however, assumed a stout bear market in bonds without assuming a reversion beyond the mean, ’70s-style bust. But a fattening discount rate is exactly how we got a 14% earnings yield on the S&P 500 some 39 years ago (figure 8), as the S&P 500 earnings yield (E/P) raced ahead of the 10-year Treasury yield from the early ’70s to the late ’70s, only to be finally “eclipsed” by a raging bond bear market thereafter.

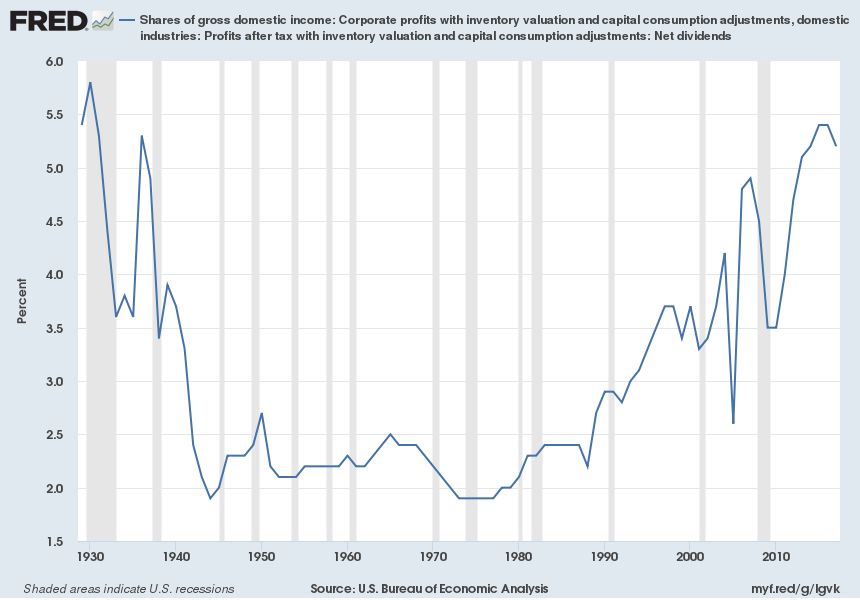

Outsized discount rate expansion (beyond benchmark interest rate increases) would be particularly true should generational “shareholder equity enchantment” morph into generational “shareholder equity disenchantment.” Disenchantment would surely beckon if rising discount rates were also accompanied by “beyond the mean reversion” of an increasingly unsustainable, 37-year rise in net US corporate profits as a percent of US domestic income (essentially the flip side of GDP; please see chart below), setting the stage for a “dual-tier” stock value compression.

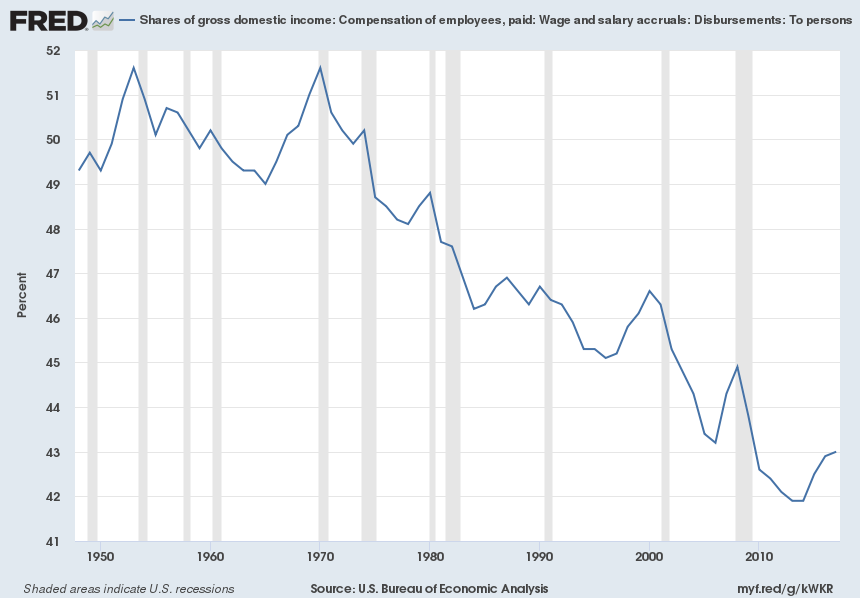

Noteworthy, and unsurprisingly, four decades of rising American corporate profits are juxtaposed against a 45-year slide in compensation of US employees as a percent of US domestic income (“labor’s share;” please see second chart below). A sustained trend reversal here — despite all the AI and robotics worker displacement/termination headlines, which frankly remind this author of how the ag revolution was going to permanently wipe out income for most Americans, most of which worked on farms at that time — would constitute secular profit pressure. This would amount to a shareholder double-whammy if accompanied by rising discount rates. (Or perhaps if machines render a huge portion of the workforce academic and thus unemployed, despite the millions of likely well-paid new jobs AI and robotics should result in, then maybe corporate taxes will need to surge to finance “universal income” or some such travesty, indirectly still leading to potentially lower corporate net profits, especially if this a global trend that renders “overseas labor outsourcing” obsolete. How does one spell “shareholder disenchantment.”)

Source: https://fred.stlouisfed.org/series/A449RE1A156NBEA

Such shareholder disenchantment, and the associated low P/Es, has happened in decades past for a decade, and sometimes considerably longer. With near-record low interest rates set to rise amidst sharply increased and absolutely unparalleled US and global solvency risks, the associated low growth risks, and much higher QE-induced misallocation and monetary inflation risks, value stock market caps should suffer less than growth stock market caps.

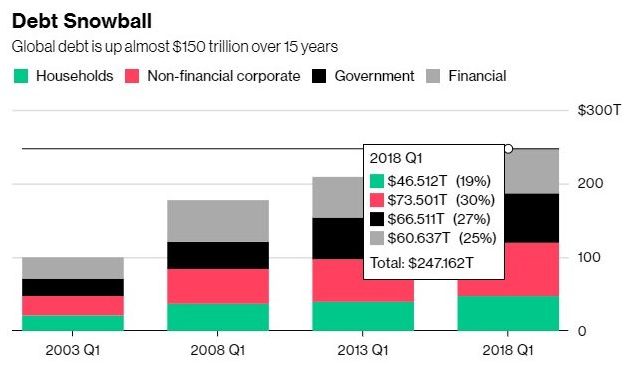

Last but not least as regards the bigger point theme, I’d be remiss if I didn’t call out the humongous dense energy availability, affordability, and misallocation challenges that could render everything else discussed here and elsewhere academic. Those same challenges threaten the very leveraged output, much less (revisiting) sustained productivity advances, that are key to enabling continued robust shareholder returns on equity and solid returns for all capital providers, including the unprecedented amounts provided by creditors, many of which represent increasingly imperiled pensioners:

Sources: Institute of International Finance and www.bloomberg.com/news/articles/2018-07-10/global-debt-topped-247-trillion-in-the-first-quarter-iif-says

Caveats and closing thoughts:

To reiterate, both EPS growth and discount rate assumptions hugely impact NPV outcomes, making intrinsic value estimates derived therefrom rather tenuous. Plus, my 6% annual “value stock” EPS compounding during the first decade is more than double the S&P 500’s track record between 2006 and 2017 in the same realm. This “reach” is obviously not well supported by history. My only weak intellectual excuses are as follows: a) “negative news” or “event-driven” value stocks (probably the majority of value stocks in a vastly over-valued US stock market) will often exit under-performing business(es), which will tend to raise company-wide EPS growth rates for a time; and b), my the value stock NPV calculation is compared against a growth stock NPV calculation in which the growth stock EPS CAGR remains at an absolute nominal GDP growth trouncing high-to-mid-double-digits rate for two decades. A hugely imperfect and arguably flawed effort at an individual security level, but perhaps at least broadly indicative of the upcoming divergence between value and growth stock price compressions in an overdue bond bear market. Both types of shares will get clocked, but value stocks, as a group, will wilt (price-wise) less than growth stocks. I’ve tabulated a 38% hit vs. 48% hit, as you know. Still ugly, but considerably less so, which is precisely the point we’re trying to make. To get back to a “100 purchase price,” that value stock price would need to rise by 61%, while the growth stock price would have to nearly double (up 92%).

Some thoughts for those that “can’t wait to buy US stocks” prior to history repeating itself.

And while we’re on the topic of history repeating itself, we’d be remiss if we didn’t mention how incredibly ridiculous and dangerous today’s intimidating, potentially career-shredding, at times financially-ruinous PC world is for those that dare to make a stand against a popular, whipped-up narrative — fair discovery, full transparency, timely charges rendered, evidence, witnesses, and facts be damned. A world in which all too often “guilt” is assumed, rather than innocence. Innocence is THE key assumption/bedrock principle underpinning due process rights, the west’s legal system, and a fair, humane governmental system. Spreading political correctness is nothing other than suppression of free speech, and thus freedom. Thought tyranny leads, inevitably, to brass-knuckle tyranny. That is, history repeats.

For disturbing “Borking” flavor on precisely the above topic, consider the absolutely contemptible effort by the deeply corrupt, purely politically-driven left to keep Judge Kavanaugh from becoming SCOTUS Justice Kavanaugh. If a “last minute” effort to derail the confirmation of a highly qualified candidate with a multi-decade track record of constitutional fidelity when rendering decisions (what judges are supposed to do, i.e., endeavor to faithfully interpret the Constitution) is successful, then we are in even deeper political trouble than is already the case. This is all the more true if an utterly isolated abuse charge, dating back 36 years (purported unwanted sexual advances by then teenager Kavanaugh) by a woman that can barely remember any of the “shirt-groping” details and only recently came forward with this claim, ends up shutting down Kavanaugh’s confirmation/nomination. Insanity would rule, and a very high profile political lynching by “the mob” would set a very dangerous precedent.

With $21trn in unaccounted for US government spending pointing to $21trn in unaccounted for money, widespread lawlessness at the highest echelons of power, an ongoing coup attempt to remove a duly-elected president from office or to totally incapacitate him, and an increasingly encompassing effort to institute de facto one-party government (by the allegedly “out of power” Democrats as enabled all too often by statist RINOs) as currently on display with the Kavanaugh confirmation circus, confidence is not being furthered and trust is not being (re)instilled. All said, such goings-on further threaten a return to a reinvigorated rule of law, which is in deep, deep trouble (throughout the west). And, for the same political reasons, our bubble valuations, which are already disconnected from financial and economic sanity, are also in deep trouble. Investors assume stout rule of law protections, including in the all-important property right arena, which have long been under attack by the courts and the bureaucracy, both domestically as well as in other OECD nations. At some point, all of the sudden, trust will wilt, and asset prices will “catch up” with political, financial, and economic reality. Perhaps Trump’s recent, yet overdue declassification of key FISA documents will prove to be the catalyst that pulverizes confidence by disclosing the unparalleled bureaucratic (deep state) lawlessness that has been taking place. Caveat: only if the declassification is actually released for public review.

Which begs the question: how can one value assets in a de facto banana republic (from a host of perspectives, including numerous, top-tier, un-indicted felons on, or previously on, the taxpayer payroll that are still at large*), versus in a rule of law republic, other than with extreme caution, i.e., via high bond yields and low P/Es, the antithesis of today’s US asset valuation bubbles? How long will the bond vigilantes, the “algos,” and the so-called market technicians remain asleep at the switch; will the spreading contagion or an expanding trade war be the trigger that flips it? Or, will we have to await a US equity market swoon before the Fed’s QT morphs into unprecedented QE? This is the $64,000 question, especially with the Fed’s QT in nearly “full-blown,” $50bn p.m. asset sale mode amidst huge and growing debt, rising deficits, and crumbling EM market currencies, bonds, and stocks. (And crumbling EM economies are no longer able to hitch a ride on the erstwhile speeding “China growth train,” as that nation’s economic locomotive role has run into a $34trn wall of debt, a tally that has led to a 266% Chinese debt to Chinese GDP ratio as of the close of 2017, up explosively from 162% in 2008.)

How long until the US stock market succumbs to political, financial, and economic “valuation reality 101” and to an increasingly dicey global economy? And will the US stock market again lead the US bond market into a full-blown bust, just as it did in the ’70s (figure 8)?

Sincerely,

Dan Kurz, CFA

* – For absolutely outrageous “over-the-top” flavor, consider Hillary Clinton. The felonious former secretary of state destroyed massive amounts of evidence while gravely violating classified information security protocols with her private servers, and thus gravely threatened national security. Yet, she was effectively exonerated by former FBI head Comey, who had the temerity to a) usurp judicial power and b), at the 14-minute mark of his self-righteous July 5th, 2016 tirade on this matter, warn that “everyday” Americans, in contrast, would be held accountable: “this is not to suggest that in similar circumstances, a person who engaged in this activity would face no consequences!” (When there are two sets of laws, one for the mighty who stand above the law, another for the rest of us who have to abide by the law, a society by definition cannot have the rule of law.)

This commentary is not intended as investment advice or as an investment recommendation. Past performance is not a guarantee of future results. Price and yield are subject to daily change and as of the specified date. Information provided is solely the opinion of the author at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Information provided has been prepared from sources deemed to be reliable but is not a complete summary or statement of all available data necessary for making an investment decision. Liquid securities can fall in value.

Post #46: End game — who fills the power vacuum after financial Armageddon? Kenneth Ameduri’s Crush the Street interview with your author

Post #45 is a DK Analytics video on global financial meltdown risks and ultimate Fed response

Post #44: America in Q4, QT, crashing foreign markets & currencies, and the ever-closer “reset”

DK Analytics, Post #44: America in Q4, QT, crashing foreign markets & currencies, and the ever-closer “reset” 8/26/2018

Trade weighted US$: 91.03; US 10-yr: 2.83%; S&P 500: 2,862; Oil: $68.72 Gold: $1,213; Silver: $14.90

Source: https://fred.stlouisfed.org/series/BAMLEMHBHYCRPIEY

Source: https://www.bloomberg.com/news/articles/2018-07-10/global-debt-topped-247-trillion-in-the-first-quarter-iif-says

It’s getting choppier:

When asked where America is headed in Q4 as a topic of discussion for a rapidly upcoming interview, I wrote back that I am less sure where America is headed in Q4 than “down the road” in general. The whole thing (political, financial, economic) could fall apart at any time. On Monday, August 27th, 2018. In a week. In a month. In a year. In a year and a half. I just don’t know, for “markets can stay irrational longer than investors can remain solvent” (Keynes said some smart stuff like that, and even he didn’t subscribe to governments’ forever rising tides of red ink, but rather applauded generating deficits only during recessions that would then turn into surpluses during recoveries, but I digress).

That said, and as per my latest post on QT, I believe the Fed’s monetary tightening will greatly hasten the “reset day.” The Fed’s sustained tightening is already causing numerous EM currencies, stocks, and bonds — trillions of which (out of $58.5trn in aggregate) are denominated in dollars, with $500bn coming due in 2019 alone — to implode. Meanwhile and concomitantly, the Fed is increasingly choking off growth in a debt-addicted US and global economy while raising EM’s financing costs in currency and interest expense terms. This is especially true as we haven’t addressed what I call a toxic public policy stew. Translation: as unelected bureaucrats, statist politicians, judicial despots, and crony capitalists remain busy killing the free market patient (esp. in the west and in India), private sector wealth creation, productivity, and good jobs, everything runs on access to (yet more) credit. Take that away or make it more expensive without removing free market capital’s growing “global corset,” and that overdue recession won’t be overdue much longer (and neither will a stock market drubbing reaching US shores).

A “run-of-the-mill” recession would be a celebratory benign outcome on the heels of decades of political, financial, and economic malfeasance by an ever more entrenched global “ruling class.” Call them oligarchs, plutocrats, fascists, lawless tyrants, or even central bankers. In any event, serfdom suits them all just fine, and they are well on the road to ruin (for the “99%”). Now, of course such “deplorable” topics weren’t discussed at the annual Jackson Hole central bank love-fest a few days back, nor will they be discussed in the Alps of Switzerland in the coming winter (otherwise known as Davos).

Carping aside, back to getting a bead on what’s going on/going down. We all know how intertwined today’s global capital and currency markets are — more than ever before thanks to globally coordinated and orchestrated “financialization.” For flavor and for a preview of coming attractions (“Deutsche Bank” and bankrupt governments), you may recall how in 2008 UBS, the “unassailable” Swiss financial titan, was nearly brought to its knees due to huge exposure to imploding US mortgage asset valuations, including $26.6bn in investment-grade “junk.” If it hadn’t been for a swift taxpayer bailout, massive fund withdrawals by UBS’s creditors and depositors would have rendered the bank both illiquid and insolvent. My point: how does one spell CONTAGION, revisited? And let us not even get bogged down in the quadrillions of dollars in derivative exposure risks by leading financial institutions, the largest chunk of which are bets that global money center banks made on interest rates staying abnormally low, despite unprecedented monetary inflation risks and/or insolvency risks (Venezuelan-style monetary debasement is just another form of insolvency or complete loss of creditors’ purchasing power). As such, if interest rates “rise from the dead,” many banks will be dead, and those parties that would have enjoyed huge profits from rising interest rates, won’t. A global financial meltdown, perhaps triggered by banks’ material exposure to rising interest rates or to escalating non-performing EM loans, wouldn’t be out of the question.

That Fed QT will morph into record Fed QE (debt monetization) amidst reversion beyond the mean:

A metastasizing contagion suggests a fairly quick and record reversion to QE by the “terrifically exposed” Fed and a return to fed funds rate cuts is just out of sight (when push comes to shove, the Fed will protect its owners’ balance sheets; those balance sheets belong to the big money center banks). When this manifests, I believe it will be the wake up call that finally makes investors smell the “traditional asset and RE bubble valuation coffee.” And once the algos go in reverse — feed on themselves in a falling market by triggering yet more sell orders — we will finally have that big, fat, overdue, and ugly reset: every asset gets repriced down relative to gold (and, by extension, silver).

Recall that markets are “reversion beyond the mean machines.” In this case, from boom valuations to bust valuations. Upshot: we should once again see single-digit P/Es and double-digit bond yields — and nasty inflation/stagflation, as a crack-up boom finally ensues on the back of some $16trn in global central balance sheet expansion over the past decade that starts to find its way into the “real economy” with a vengeance (recall that central bankers have been desperately trying to stoke more inflation, and that once inflation starts, it typically gets out of control). Arguably, we’ve never had so far to fall, globally speaking, because we’ve never had each major currency utterly divorced from any kind of defensible precious metals backing and discipline (although this could be on the verge of changing in both Russia and China with precarious implications for the greenback, especially if Germany wants a viable global reserve currency alternative to the buck), which has gotten us into all sorts of political, financial (debt), and economic trouble. Not a good time to have asset valuation acrophobia.

We are so close to numerous remaining bubble asset valuation implosions, and President Trump’s trade antics and/or heightened political instability in the US and in EM, from South Africa to Turkey to Iran to Venezuela, threaten to make the global reset “closer still.” Why? Because increasing political uncertainty and tariff wars will “kill” already globally weak economies facing the headwind of rising debt-induced interest expense growth prior to any interest rate normalization, much less “overshoot.” After a 37-year bond bull market, one can almost hear the rumbling, even at the dollar-based center of global finance.

In the interim, the rule of law is virtually dead in the US and the West, and the un-elected, statist bureaucratic chieftains, with their powerful, protected jobs and their well-paid, ever-growing staffs (over 2m civilian bureaucrats in the US alone), have successfully usurped legislative prerogatives from elected officials — specifically, from the Congress in the US and from parliaments in Europe. This, coupled with legislating from the bench, has not only effectively ended representative government in many OECD nations, but it has eviscerated working citizens’ property right protections, free market capitalism, productivity, and numerous nations’ balance sheets: at nearly $250trn in operations-based debt, the globe’s $81trn economy is too encumbered for anything but a destructive debt-based deflation. That deflation will be fought tooth and nail with the printing press for political reasons until fiat money and its purchasing power are totally destroyed, as has always happened.

Simultaneously and sadly, unless reversed in time, many western nations’ sovereignty, cultures, codified individual freedoms, and tolerance will also be balkanized away. Needless to say, budding resistance to this destructive status quo is resulting in growing political divides, which in turn is fueling rising tensions and potentially destabilizing political situations from Italy to the UK to the United States. If this continues to ratchet up, as “populists”/workers increasingly clash with leftists/globalists, this could yield political paralyses, constitutional crises, and/or, in a worst case scenario, anarchy or war. Needless to say, all of them would pressure stock, bond, and real estate valuations, including in “safe haven” America.

Speaking of America, the buck and the US stock market, which have been rallying as many ROW currencies and equity markets come under substantial pressure, are arguably the biggest, most unsustainable, and most foreign capital and import dependent bubbles of all (and of all time). Ultimately, the US, the world’s largest net debtor nation ever (nearly $8trn) — a nation long lacking robust domestic savings that may well be looking for between $2trn – $3trn in new net financing p.a. given its current trajectory, which a stouter recession would widen substantially — cannot possibly have a sustainably strong currency. Said is all the more true if that nation’s central bank appears bent on driving an economy still caught in a Fed-enabled bureaucratic and litigation (red tape) straight jacket, and way overdue to enter an “official recession,” right off the cliff.

They say that all politics is local. And that everything is political. Well, when the Keynesian-overkill dolts or the central planners/monetary despots (pick your poison) running the Fed figure out that their owners are not going to be happy nor as rich on the heels of America’s stock bubble getting pricked (been there, done that in ’08, and this time around taxpayer-funded, TARP-style bankster bailouts are allegedly off the table), they will quickly resort to the only tools in their fiat currency toolkit: revisiting QE and a rapid trip back to ZIRP from a still pathetically low fed funds rate. And, by the way, that 1.9% effective rate amounts to a negative real rate. This is true either using fake government inflation stats pointing to 2.9% inflation currently, or if looking at a more credible estimate of inflation running between 6% – 8%.

The Fed’s (and other leading central banks’) doubling down on financial repression anew will prove what a big, fat, and ugly failure their policy of financial cocaine has been. Economic (productivity) devastation. A dwindling middle class. Ever greater, increasingly unheard of, and (often) cronyism-induced wealth concentration. Yet, most ironically, even more QE will be required given that the economy is drowning in the very debt that the central bankers have enabled. Plus, politicians can’t go cold turkey without getting fired at the ballot box (let’s not forget increasingly imperiled pension plans) and central banks will protect, well, banks. And that last man standing, the USD? It will be naked. Not such a pleasant sight, especially when considering dollar-based assets.

At such a juncture, which we view as imminent, even the most clueless deniers will have to realize that we are now irreversibly and increasingly quickly on the path to complete global fiat currency destruction — and that all assets deriving their value from being tethered to unbacked currencies will be “collateral damage.” Most stocks, but especially bonds given “repayment impossibilities,” are going to get killed. Global printing press-led currency devaluation contests will sprout once the 800-lb Fed re-enters official currency debasement. A budding trade war would only add fuel to the fire.

What to do as the reset can be seen on the horizon:

Silver and gold (real money for thousands of years), and other vital real assets, starting with the dense energy and ag complexes, will be good places to seek huge purchasing power gains as well as purchasing power protection. Reasons: precious metals are money and dense energy and ag assets are increasingly scarce/can’t be printed, and they remain vital both to leveraged output and sustaining 7.2bn people’s lives.

Meanwhile, select short-term government bonds, such as US T-Bills, will be good places to hide pending emergence of true bond, stock, and real estate bargains. The reason: governments can print the money to repay these bonds. Plus, short-term government bonds avoid both interest rate risks and bank bail-in risks. There is bail-in legislation in place throughout the OECD world that will have your bank deposits converted into bank equity of very questionable value if necessity dictates, which could happen as taxpayer bailouts are, well, out. You didn’t intend to buy bank shares with option-like valuations with your money, did you?

Speaking of which, avoid bank illiquidity risks. And remember something about that bank account of yours: your deposited funds represent unsecured (junior) creditor claims! With banks typically investing over 95% of depositor funds and depositors typically representing well over 50% of bank financing, you want to limit your exposure here, FDIC insurance protection notwithstanding. Reason: the FDIC’s funds would cover only 2% of insured deposits. Moreover, deposits at risk can’t be money, right, because money is supposed to be both without risk and without yield?! While your bank accounts or money market accounts are virtually without yield (and devoid of a real yield), they certainly aren’t without risk, so why not shift excess (beyond working capital needs) funds into short-term (two or three month) government bonds?

In closing, let me now revert to the opening question, namely where is America heading in Q4? Once again, I don’t know where America will be in Q4. As regards a reset (in dollar and all fiat currency terms, massively lower bond, stock, and real estate values juxtaposed against substantially higher precious metals prices and, over time, materially higher scarce vital asset prices), it could be earlier or later. That said, I would state that America’s currency and America’s bond and stock markets will be heading where much of the world has been heading, especially the EM, because the whole world is basically in the same leaky political, financial, and economic boat. It would not surprise me if a US-based reset started to develop prior to year’s (2018’s) end. Once it starts, a rout will be difficult to stem. By contrast, it would surprise me greatly in today’s globally intertwined financial and economic world if the wheels didn’t come off the current American valuation bus by next year, especially given mounting confidence (political) and economic challenges, very much including an overdue recession.

We live in “exciting times” full of risks and opportunities of a possibly once-in-a-lifetime nature. That quiet before the storm, that “big fat eye of the hurricane” that I mentioned in March numerous times via various publications, could be departing. Consider reallocating. Afterwards, brace for up to 156 mph/251 km/h wind speed, or a category 5 financial storm. And then back up the truck. But don’t rush. Ultimately, unbelievable bargains will be available that most won’t consider in bonds, in stocks (and entire businesses), and in real estate. Reminds me of precious metals today.

Sincerely,

Dan Kurz, CFA

This commentary is not intended as investment advice or as an investment recommendation. Past performance is not a guarantee of future results. Price and yield are subject to daily change and as of the specified date. Information provided is solely the opinion of the author at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Information provided has been prepared from sources deemed to be reliable but is not a complete summary or statement of all available data necessary for making an investment decision. Liquid securities can fall in value.

Post #43 is a DK Analytics video on Q2 US GDP growth & QT; if it ramps to $600bn, look for accelerated “reset”

Post #42: If QT keeps ramping up to $600bn, look for an accelerated “reset”

DK Analytics, Post #42: If QT keeps ramping up to $600bn, look for an accelerated “reset” 7/14/2018

Trade weighted US$: 89.58; US 10-yr: 2.83%; S&P 500: 2,801; Oil: $70.58; Gold: $1,242; Silver: $15.84

YOY (year-over-year) change in monetary base as per 7/5/2018: –$84bn

Growing financing needs juxtaposed against a shrinking Fed balance sheet (“QT”) spell trouble:

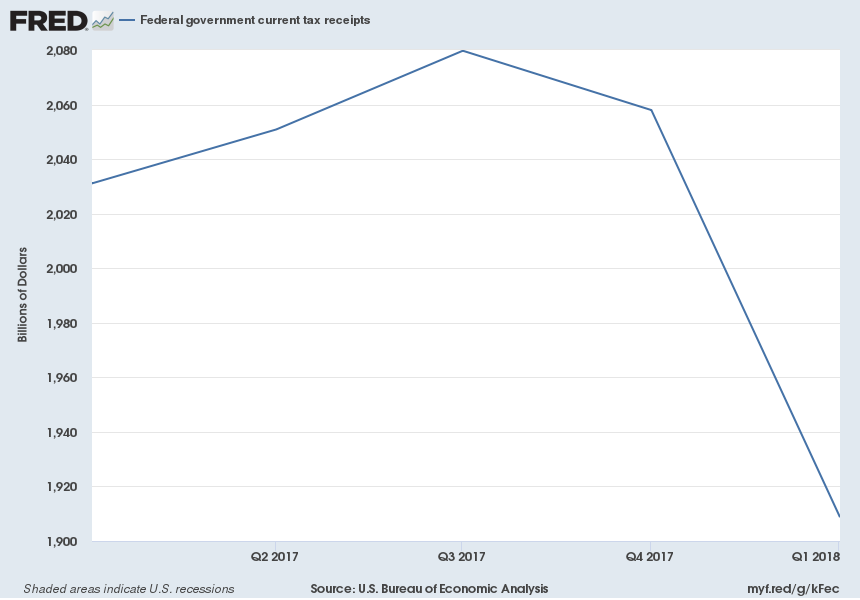

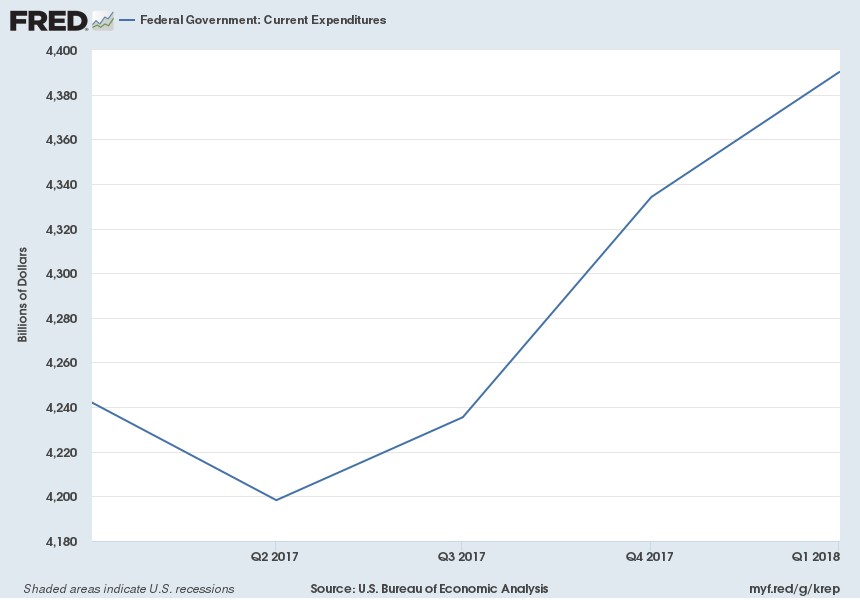

- The $1.36trn YOY increase in US federal debt through 7/6/2018 is not only indicative of the true deficit, but it is up from a $501bn increase over the 12 months ended 7/6/2017. The $860bn expansion in the federal government deficit, which reflects an expanding gap between US government receipts and spending, will mushroom in a weakening economy featuring lower tax receipts and higher social safety net spending such as jobless and welfare benefits.

- (Calendar YTD, federal debt is up by $715bn.)

Sources: https://fred.stlouisfed.org/series/W006RC1Q027SBEA & https://fred.stlouisfed.org/series/FGEXPND

- In fact, if the last recession is any guide, and given today’s even more pressing economic and financial concerns, the current federal deficit could easily bloat by $1.25trn. Washington having to potentially fund a $2.6trn plus annual deficit via new debt (Treasury) offerings would constitute unprecedented supply hitting the bond market.

- The “Treasury’s” current outstanding debt of $21.2trn has an average weighted maturity of 5.9 years. Upshot: on top of a rapidly expanding US government deficit, on average about $3.6trn needs to be refinanced annually.

- An ever-more indebted economy can ill-afford higher interest rates, much less a recession. With total US debt already expanding at a $2.6trn annual rate and closing in on $69trn, which amounts to 3.4x GDP, a one percentage point (100 BPs) rise in the 10-year Treasury (“benchmark”) yield would reverberate throughout the “debt structure landscape,” starting with the public sector. This is because a substantial portion of outstanding debt in both consumer and corporate loan realms is tied to the benchmark yield plus a risk premium. As investors seek greater “solvency protection (max time frame),” private sector interest rates will surge thanks to widening risk premiums or “spreads.” Let us take a “back of the envelope” stab at the implications of a rising benchmark yield:

- Let’s assume, for the sake of argument, a 5.9-year average maturity for “all US debt” (it may be longer or shorter, given outstanding “Treasury Yield Plus” household loans of shorter durations, shorter and longer corporate liabilities, and 7% homeownership turnover rates superimposed on 15 and 30-year mortgage refis).

- In such a world, some $11.6trn of refinancing ($68.6trn/5.9 years) would coalesce with an assumed $2.6trn plus in new debt issuance at a higher interest rate.

- With about 69% of all American debt consisting of non-US government debt (US debt service is supported by a printing press thus is less risky, in nominal terms), a 100 BPs higher Treasury yield could easily result in the cost of much of the other debt (including state, corporate, and household liabilities) rising, in aggregate, at 1.5x – 2.0x the benchmark yield increase, for a “blended rate” increase of some 1.5 percentage points, or 150 BPs. (Swelling debt growth and a $16trn higher debt load than a decade ago may result in a higher “blended rate,” much as elevated monetary debasement risks may push the Treasury yield higher.)

- Thus, $11.6trn of refinancing per 100 BP rise in the benchmark rate could easily result in $174bn higher refinancing cost (for outstanding debt) per annum for America.

- Toss in an additional $111bn in interest expense for $2.6trn in new annual debt issuance, and America could loosely be looking at a $285bn ($111bn + $174bn) annual “step-up” in financing costs that would roll out for some six years assuming solely a 100 BP increase in the benchmark rate combined with annual debt growth.

- Over six years, that could spell $1.7trn in higher annual financing costs, or 8.5% of current GDP.

- Talk about cost of funds headwind prior to any interest rate “reversion beyond the mean,” much less interest rates reaching average levels (a 4.6% benchmark yield), which could raise the annual financing cost bogey to $486bn.

A potential annual barrage of $2.6trn plus in new total US debt issuance coupled with $600bn in annual debt securities sales targeted by the Fed amidst a) rising liquidity issues in a budding recession, b) mounting private sector and state-level solvency concerns, and c) a concerted global effort to reduce reliance on the dollar in global trade collectively suggest that a surge of US debt coming to market will overwhelm demand at current yields. Said differently, higher returns/yields will be sought by investors — likely much higher yields, especially from today’s near-historically low levels.

Meanwhile, weaker US economic indicators add another layer of uncertainty:

- Sinking productivity growth threatens profits and payrolls alike.

- The personal savings rate, near a 59-year low, keeps falling, limiting consumers’ ability to spend (out of an empty pocket).

- (An 8/31/18 note: the BEA arbitrarily doubled the personal savings rate after this post! Call it a blast from the 2014 past, when the personal savings rate that had been calculated since 2007 as more than doubled, retroactively. More “politically acceptable” numbers magic! No more negative savings rates. Presto. (Similar “magic” has long been been taking place other macro stats such as unemployment, inflation, real GDP, and, by extension, productivity tabulations.)

- A low labor force participation rate and high “real” unemployment (if all discouraged workers were included) further restrict spending vitality, especially given the rise in household debt to a new all-time high of $13.2trn.

- Falling consumer confidence suggests a reduced spending proclivity going forward.

- Higher oil prices/rising pump prices are sapping consumers’ non-transportation spending capacity.

- Industrial production, which is currently below its 2007 high, could be topping out, especially if tariffs keep rising.

Plus, the 2018 US fall election suggests the Fed could suddenly put back on its political hat:

Under Obama, the Fed raised the fed funds rate only once. Under Trump, the rate has been hiked six times. Trump nominated the new Fed chairman, Keynesian Jerome Powell, last November. Midterm elections are around the corner even as the economy is losing steam amidst rising, and perhaps metastasizing, geopolitical — trade war — risks. Could this provide the Fed with the perfect rationalization, even prior to a stock market rout, to revisit its rate and QE toolkit (and surely the Fed would seek to re-inflate a key yield starvation offspring, a pricked equity bubble)? Moreover, the Fed tends to support the party in power, especially if the chairman has been appointed by a sitting president.

Conclusion — it is high noon head for a restrictive Fed amidst an “ecosystem” rushing to the ER:

The Fed has effectively been tightening since it started to reduce its monthly QE as of December 2013, only to end its bond purchases completely in October 2014. Cessation of QE has been augmented by an interest rate tightening cycle since 2016. Now, despite a) unprecedented and growing governmental, corporate, and household debt mountains, b) huge policy-induced distortions and misallocations, c) drooping productivity, d) very poor real wage growth (most new jobs have been low-paying, non-benefit, part-time in nature), and e) a long-overdue “official” recession, the Fed is desperately trying to raise rates enough to be able to lower them! In so doing, a government-defined recession will be hastened, and asset bubbles endangered.

That same Fed is also seeking a reduction of its unparalleled balance sheet so that it can again be expanded when necessity dictates it (protecting the balance sheets of its owners, the money center banks) and politics mandate it. In a nutshell, the Fed appears determined to take away its “cocaine and heroin” and push an economy with the albatross of a toxic public policy stew around its neck (financial repression-enabled statism, cronyism, and redistributionism amidst sustained property rights-shredding, cronyism-abetting regulatory and litigation insanity) over the edge so the Fed “can save it again.”

If the Fed continues its restrictive trajectory both on the interest rate (fed funds rate) and on the QT/bond sales front, it is virtually assuring that the fabricated and overstated economic recovery will implode even sooner. That very reality, coupled with the fact that other major central banks, such as the ECB and the BOE, have just commenced shifts to more restrictive monetary policies, suggests that a forced US monetary loosening could well occur just as a (likely fleeting) monetary tightening occurs elsewhere. An unexpected dollar rout would quickly develop.

Perhaps the yield curve, which is close to inverting, will be our single best guide as to when the Fed needs to “smell the ease ASAP coffee.” An inverted yield curve is a well-known precursor of a recession, having predicted all nine US recessions since 1955 with a lag time of six months to two years. Given America’s fragile economy, …

Talk about a perfect revaluation storm — the dollar down, bonds down (pages 8–9), stocks down, and precious metals up — in the making, otherwise also known as a “reset.”

Or, as a brilliant macro analyst from London so precisely retorted during a recent email exchange:

Your author’s comment to the macro analyst:

A German once nailed it about 25 years ago at a Rubbermaid road show in Zurich. He said to me: “you Americans focus on getting the stock price up, we Germans focus on getting our products right.”

There’s more than a speck of truth to that!

That sage analyst’s response:

Agreed. A good product is the real value. The rest is just a distraction.

The takeaway: the value of a nation’s currency will ultimately reflect a nation’s competitiveness in the global marketplace. Bonds are “currency promises.” And stocks are linked to bonds. Meanwhile, all price manipulations eventually end, and over the long pull precious metals (PM) protect purchasing power against both the ravages of deflation and inflation. Call PM a current “double-dip” satellite allocation opportunity. The likely PM price “uncorking:” a sprightly and unexpected shift from QT back to possibly unparalleled QE by the Fed. The irony that this would be triggered by a Fed-hastened reset will be hard to miss. The good news: “Frankenstein Finance” can be capitalized on.

Sincerely,

Dan Kurz, CFA

This commentary is not intended as investment advice or as an investment recommendation. Past performance is not a guarantee of future results. Price and yield are subject to daily change and as of the specified date. Information provided is solely the opinion of the author at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Information provided has been prepared from sources deemed to be reliable but is not a complete summary or statement of all available data necessary for making an investment decision. Liquid securities can fall in value.

Post #41: Trump, the “real US worker deal” and Hooverism, revisited?

DK Analytics, Post #41: Trump, the “real US worker deal” and Hooverism, revisited? 7/4/2018

Trade weighted US$: 89.97; US 10-yr: 2.83%; S&P 500: 2,713; Oil: $73.64; Gold: $1,256; Silver: $16.08

The good:

“Red state” Americans, yours truly included, are grateful that President Trump is calling out the fake news for what it is: fake — and out to get any powerbrokers that threaten its pervasive media dominance. Clearly, a media with a revolving-door to bureaucrats has facilitated unprecedented industry consolidation since President Clinton signed the Telecommunications Act of 1996. The increasingly incestuous, oligopolistic relationship between big government and big business has resulted in a crony press that rivals the Pravda (“truth”) press in the former USSR. Thus, instead of news and a check on increasingly abusive government power, as the Framers intended, the misnamed “Main Stream Media” (MSM) has been generating propaganda supportive of an increasingly fascist regime, i.e., the US government.

Billionaire real estate and successful entertainment tycoon Donald Trump refused to become part of today’s MSM quid pro quo. He didn’t have to, nor did he want to. Instead, he took his “America First” (including bringing jobs back home) message to “flyover country” via the Internet/his Twitter account and as supplemented by his frequent, rousing, and well-attended speeches. Critically, he was also backed by the one largely anti-leftist entity in the MSM, ratings dominating Fox News, which has long resonated with “red state” Americans. Thus, the battle lines were drawn. An all-out MSM backlash against this nonconformist ensued, and “news” morphed even more completely into statist, anti-Trump propaganda, a.k,a., fake news. It wasn’t only fabricated stories, one-sided allegations or quotes taken out of context, but utter and complete suppression by the vast majority of the MSM of lawless behavior by those positioned at the top echelons of federal power during the prior administration as well as unconstitutional behavior being carried forward into the current administration and into the 115th US Congress.

The Trump administration, however compromised, appears to be making a largely clandestine effort (via sealed indictments) to smoke out the “deep state” (the unelected bureaucracy and its hangers-on both inside and outside the government) lawlessness that it has been a victim of. Any success here, no matter how unlikely given the de facto “broad daylight conspiracy” — criminal decision makers keeping quiet buttressed by their staffs wanting to maintain the huge bureaucracy’s unconstitutional power, their outsized compensation, and their privileged benefits status quo — would be monumental. Such an achievement could spark a rule of law revival, arresting our B.R. trajectory. Meanwhile, a strategic return to greater constitutional fidelity is getting a sorely needed lift by Trump’s fine judge/justice selections!

The bad:

Trump’s integrity. Is it there, when it counts, beyond his stellar judge selections and beyond the fact that he isn’t an “unindicted felon,” i.e., Hillary Clinton? This isn’t an idle concern, for integrity begets and nourishes credibility, which is critical to a president’s “bully pulpit” efficacy in “troubled times.” Some worrisome signs include:

- His real estate developer exploitation of the property rights-curdling Kelo vs. New London decision suggests neither fidelity to a constitutional anchor (property rights are tied at the hip to liberty) nor to the lot of everyday Americans.

- His tabloidesque remarks about Ted Cruz’s dad being involved in the JFK assassination give further pause.

- His debate claim of putting Hillary in jail if he’s elected only to pathetically comment, once president-elect, that “Hillary Clinton had suffered enough” is disingenuous at best.

- His apt campaign claims that the low unemployment rate was fake, the recovery was the weakest ever, and the stock market was a bubble susceptible to an interest rate spike morphed into the lowest unemployment rate since the turn of the century, the best economy ever, and the best stock market ever once he sat in the oval office.

- From vowing to crack down on illegal immigration and erecting a wall on the southern border, Trump’s 1.8m “pre-wall” amnesty proposal threatens to effectively “green-light” the very illegal, third world immigration that has led to a massive transfer of property from citizens to aliens while thwarting wages and Balkanizing America.

- From railing against Goldman Sachs cronyism and globalism on the campaign trail to a GS-laced Trump cabinet!

- From vowing to shrink the federal government once elected, Trump signed legislation which further bloats it.

- Instead of being honest about the long, tough road ahead to bring America back to manufacturing strength (reindustrialization takes time!), Trump has preferred exerting unconstitutional pressure on select manufacturers to highlight US job preservation thanks to his intervention, even as a closer look at such “agreements” disclosed heightened taxpayer expense and producers’ expanded outsourcing options. How does one spell “demagoguery?”

The ugly:

A potential Trump trade war is a huge risk to both the US and the global economy, but the US is especially vulnerable. This is due to America’s largely self-inflicted manufacturing enfeeblement, its huge net dependence on foreign goods (just go to WalMart’s non-grocery aisles) and foreign financing, and its dependence on continued widespread overseas acceptance of dollar-based trade, … despite America’s $7.9trn net debtor status vis-à-vis the rest of the world, over $21trn in US debt, and the US’s decade-long $1trn plus average yearly expansion in federal debt. Some reflections:

- Is Trump going the Hoover route (dangerous “interventionism” and an escalating trade war)? Hoover was a leading industrialist before he became president. Are we about to revisit this dark chapter in history?

- A nation that has an $800bn plus annual deficit in goods trade and has lost a vital portion of its manufacturing base can ill afford to start a trade war, from consumers’ or producers’ perspectives. It needs component parts that are often made only overseas nowadays (think the “787” or US-assembled cars) to produce high-value added finished products for domestic consumption and for exports, much less give it the ability to restore a domestic supplier base and address destructive corporate governance and compensation (more below).

- Tariffs are taxes on Americans that the feds collect – we thought Trump was about shrinking government?

- Protectionism (tariffs) is the worst form of cronyism: domestic steel and aluminum shareholders and their “Wilbur Ross cronies” will do fine, but domestic manufacturers of Maytag washers, Ford trucks, Harley Davidson motorcycles, GE locomotives, CAT dozers, Carrier chillers, etc. (and their workforces) will be negatively impacted or worse (bankruptcy). This is thanks to the resulting uncompetitive materials costs and/or retail prices that are out of consumers’ reach both domestically and in export markets, where outfits such as Harley will face a one-two punch of higher domestic steel and aluminum prices and tit-for-tat import tariffs for US made bikes.

- Trump should solely be talking up lowering tariffs globally — e.g., seeking Mexico’s zero tariffs to 44 nations.

- As is widely known, our top brass corporate compensation structure (CEO compensation was some 20x the average worker in 1965 and 271x in 2016), including $7m CEO signing bonuses and relatively rapid vesting of untold millions of underpriced options, coupled with litigation and regulatory insanity have come together to yield a “slash & burn” business model. In today’s world, the C-Suite a) no longer has parallel strategic organic growth interests (p. 5) with American workers, taxpayers, and communities, b) is incentivized to cut/gut domestic cap ex instead of investing, and c) is motivated to outsource and fire domestically instead of hiring and training American workers. Today’s senior management is rewarded for slashing costs while buying back stock with both cash flow and by issuing trillions in new debt to give EPS a “financial engineering lift.” The C-Suite focus: drive up the stock price ASAP instead of focusing on building globally competitive products, which is an unending effort. As such, “corporate anorexia“ has become the destructive norm. Coupled with lacking trade schools, a failing education system, and perpetually large government deficits, these are the true flies in the ointment!

{kind=link}

Unfortunately, such truths don’t make for great soundbites, but they remain truths. Plus, other high-wage workforces (with generally better paid workers than in the US) operating in generally strong currency nations — e.g., Switzerland, Germany, and, for a long time, Japan — have generated sustained and substantial trade surpluses of recent vintage that sometimes extended for decades, and typically included surpluses with China.

Commensurately, those that blame high US wages or a strong buck as “America’s chief culprits” are just not getting the big picture right, much less how to best address it: with “brick-by-brick” home-grown solutions (for largely home-made problems) instead of with misleading, silly, and patronizing claims of having (virtually) instantly “made America great again!” Moreover, reputational integrity does matter when a president is attempting to make constructive deals for his country. Yes, Virginia, both policy and integrity (character) matter.

Allocation conclusion:

If, against all odds, the rule of law is restored in the US and the lawless actors infesting the governing class/controlling the instrumentalities of power are brought to justice, the profound and breath-takingly stunning “gravity of it all” would rapidly turn greed into fear in terms of so-called “traditional asset” valuations. In other words, sales would drive risk premiums much higher and net present values much lower, pricking today’s “bubble valuations.”

In the meantime, the US government’s reckless, deficitary fiscal policy would be even more exposed in a GDP-pummeling trade war — we are already way overdue for a recession amidst a historically weak, waning-productivity, debt-encumbered, artificial recovery. Huge US commitments, political calculations, and a fiat currency — “The US can pay any debt …, it just can’t guarantee purchasing power” — could result in unprecedented amounts of dollar printing. It appears to be more a question of “when” rather than “if.” This suggests that the buck will be sacrificed in a tactical attempt to protect money center bank balance sheets (and the Fed itself) from “valuation meltdowns” and to meet “nominal dollar commitments” of a strategic nature. Monetization of debt would become permanent and be expanded upon. How does one spell “doubling-down on currency debasement?” Against this backdrop, it is hard to imagine a secularly more bullish case for undervalued precious metals — and a more opportune time to reduce exposure to massively overvalued bonds and stocks. (And please recall, markets are “reversion beyond the mean machines!”)

Finally, it is fitting indeed, on Independence Day, that we celebrate America’s historical blueprints — The Declaration of Independence, which led to the first-ever strict enumeration of governmental powers and codification of individual liberty and inalienable rights, otherwise known as the US Constitution, including the Bill of Rights. How appropriate that Americans, and proponents of codified freedom around the globe, still have the unique opportunity to fortify their financial fortunes with the very “constitutional money” that could prove pivotal in the challenging times ahead in terms of supporting their families and in terms of helping to rebuild a return to free market capitalism and constitutionalism. An increasing number of originalist/constitutional judges should be of strategic help. Thank you, Mr. President.

Sincerely,

Dan Kurz, CFA

This commentary is not intended as investment advice or as an investment recommendation. Past performance is not a guarantee of future results. Price and yield are subject to daily change and as of the specified date. Information provided is solely the opinion of the author at the time of writing. Nothing in the commentary should be construed as a solicitation to buy or sell securities. Information provided has been prepared from sources deemed to be reliable but is not a complete summary or statement of all available data necessary for making an investment decision. Liquid securities can fall in value.